IRR iç getiri oranı. Formül ve hesaplama örneği

IRR hesaplama formülü, yatırım projelerinin göreli karlılığını analiz etmek için kullanılır. IRR, yalnızca projeleri kârlılığa göre karşılaştırmaya değil, aynı zamanda piyasadaki diğer varlıklara da izin verir.

İç verim oranının ekonomik anlamı

IRR ayrıca iç getiri oranı veya IRR olarak da adlandırılır. Gelirin mutlak değerini değil, göreceli değerini değerlendirecek bir göstergeye duyulan ihtiyaç anlaşılabilir - bu değeri alıp tahvil getirisi, mevduat getirisi olsun, piyasadaki tüm olası oranlarla karşılaştırmak çok uygundur. veya kredilerin maliyeti. Varlık getiri oranlarının proje oranından ne kadar yüksek veya düşük olduğunu görerek, kendi fonlarının yatırımına karar vermek kolaydır. Aynı zamanda, getiri ve fonlama maliyetini karşılaştırarak, getiri oranı kredinin maliyetini önemli ölçüde aşarsa, ödünç alınan fonlarla bir proje başlatma kararı vermek de kolaydır.

Böylece, IRR'yi hesaplama formülü, projenin etkin kaldığı maksimum sermaye maliyetini, yani saptığı eşik oranını tahmin etme ihtiyacını çözer. Bu oran, net bugünkü değeri sıfıra ayarlamalıdır. NBD .

Uygulamada, bu göstergeye projenin güvenlik marjı denir, çünkü IRR ile sermaye maliyeti arasındaki boşluk, projenin ne kadar daha fazla krediye (veya başka türde bir finansmana) dayanabileceğini gösterir. Proje göstergesinin değeri şirket için sermaye maliyetinden (yani WACC) büyükse, o zaman kabul edilmelidir.

IRR Hesaplama Formülü

Grafik belirleme yöntemi

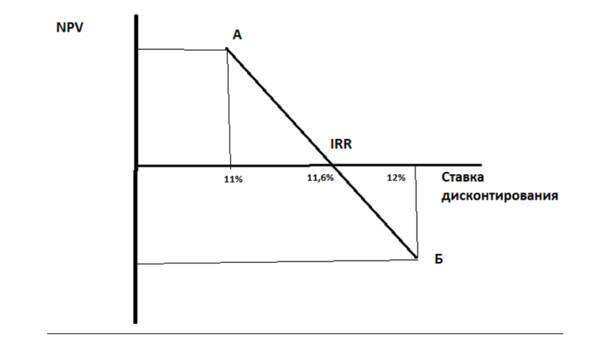

Resim 1

Bir koordinat sistemi (Şekil 1) oluşturuyoruz, burada ordinat ekseni boyunca fonksiyonun değeri NPV ve apsis ekseni boyunca - iskonto oranları. İki indirim oranı seçiyoruz, böylece bir oranda ("A" noktasında) NPV değeri pozitif, diğerinde - "B" noktasında - negatif, NPV değeri aşağıdan ve yukarıdan sıfıra yaklaştıkça, daha fazla kesin çözüm olacaktır. Grafikteki iki noktayı bir segment ile birleştirelim - segmentin apsis ekseni ile kesişme noktası, iç getiri oranıdır. Örneğimizde “A” noktasında %11, “B” noktasında %12 iskonto oranımız varsa apsis ekseninin kesiştiği noktada oran yaklaşık olarak (gözle) 11,6'dır. %. Bu kesin bir yöntem olmamakla birlikte iç verim oranının değeri hakkında fikir vermektedir.

Hesaplama yöntemi

IRR'yi hesaplama formülü ile daha doğru bir çözüm verilir:

IRR \u003d r1 + NPV1 x (r2 - r1) / (NPV1 - NPV2),

burada r1, NPV1'in hesaplanan pozitif değerine karşılık gelen seçim yöntemiyle belirlenen iskonto oranıdır,

r2, NPV2'nin hesaplanan negatif değerine karşılık gelen, seçim yöntemiyle belirlenen iskonto oranıdır.

Örneğimizde, r1 = %11, r2 = %12. NPV1 = 120, NPV2 = -90 varsayalım, ardından:

IRR = %11 + 120 x (%12 - %11) / (120- (-90)) = 0,11 + 120 x (0,01) / 210 = 0,11 + 0,0057 = 0,1157 veya %11,57.

IRR Hesaplama Problemleri ve Çözümleri

IRR hesaplama formülünün dikkate alınması gereken dezavantajları vardır. Dolayısıyla, NPV değerinin işaretinde herhangi bir değişiklik yoksa gösterge mevcut değildir. Bu, proje yatırım aşamasında kırmızıya gitmeden hemen kar ederse, böyle bir projenin IRR'si olmayacağı anlamına gelir. Durum nadirdir, ancak oldukça olasıdır, örneğin, hesaplama aralığı bir yılsa ve negatif nakit akışı yalnızca ilk aylarda ortaya çıkıyorsa ve yılın sonunda proje pozitif bölgedeyse. Hesaplamanın grafik gösteriminde, NPV değişiminin yörüngesinin, iskonto oranının herhangi bir değeri için asla x eksenini geçmediğini göreceğiz.

Bir dakika ye. Formülümüze göre hesaplanan gösterge fevkalade büyük değerler alabilir. Bu seçenek, örneğin ilk yatırımın boyutu büyük değilse ve NPV hızla artıyorsa da mümkündür.

Birkaç IRR değeri olması mümkündür, bu, örneğin proje bir dönüm noktasıysa ve büyük enjeksiyonlar gerektiriyorsa, iş modelinin farklı zaman dilimlerinde NPV göstergesinde birden fazla sıfır geçişine (işaret değişiklikleri) yol açtığı bir durumdur. proje uygulaması sırasında biriken fonları aşan. Bu durumda iç verim oranı anlamsızdır.

Ana dezavantaj, formülün yapısında pozitif nakit akışlarının iç getiri oranı üzerinden projeye yeniden yatırıldığını varsaymasıdır0

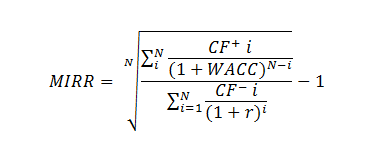

Değiştirilmiş IRR formülünü (değiştirilmiş dahili getiri oranı, MIRR) kullanarak sorunu çözebilirsiniz:

CF + - i'inci dönem projesinin gelen nakit akışları,

CF - - i'inci dönem projesinin giden nakit akışları,

WACC - ağırlıklı ortalama sermaye maliyeti (normatif getiri),

N, projenin süresidir.

Proje finansman kaynağının fiyatı üzerinden gerçekleştirilen giden akışlara iskonto uygulanır. Nakit girişlerine birikim uygulanır - projenin tamamlandığı zamana akışın maliyetini getirirler. Biriktirme, yeniden yatırım düzeyine eşit bir faiz oranında gerçekleştirilir.

MIRR, hem çoklu IRR sorununu hem de yeniden yatırılan akışların yetersiz değerlemesini çözer.

Yerleşik MS Excel araç seti, MIRR'yi hesaplamak için MIRR() işlevini içerir.

MIRR iskonto oranı - r'den büyükse, proje verimlidir ve uygulanmalıdır.

Nakit akışlarının aylık bir dökümü kullanılıyorsa, IRR'nin hesaplanmasında genellikle bir hata vardır. Bu durumda IRR() fonksiyonu kullanılarak elde edilen oranın projenin IRR'si olarak kullanılması yanlıştır. Alınan IRR oranını bir yıldaki ay sayısıyla - 12 * IRR ayı - çarpmak da bir hatadır. Aylık hesaplama doğru bir şekilde yıllık eşdeğere dönüştürülmelidir - yerleşik Excel araç seti kullanılarak hesaplanan IRR'ye bileşik faiz formülü uygulanmalıdır, ardından doğru değerini göreceğiz. Aylık nakit akışlarının dökümü için doğru formül şu şekildedir: (1+IRR aylık) 12 -1,

burada IRR, hesaplanan Excel değeridir. Üç aylık döküm için sırasıyla (1+IRR qt) 4 -1.

Genel durumda, IRR'yi WACC ile karşılaştırarak bağımlılıkları elde ederiz:

IRR, WACC'den daha büyük - proje kabul edilmeye ve finanse edilmeye değer;

IRR, WACC'den daha düşük - proje zarar getirecek ve terk edilmelidir;

IRR, WACC'ye eşittir - projenin tamamlanması veya anahtar parametrelerin değiştirilmesi gerekiyor.

Özet

IRR, ana görevi yönetime projenin finansman kaynaklarının kârsız olmadığı maksimum maliyetinin bir tahminini sağlamak olan proje performansının göreli bir göstergesidir.

Gösterge yetersiz ve çelişkili tahminler verebilir (aşırı yüksek değerler, negatif proje nakit akışı değerlerinin yokluğunda IRR olmaması, çoklu IRR'ler) ve bu durumda modernize edilmesi veya doğru yorumlanması gerekir.

IRR'yi yatırımların etkinliğinin bağımsız ve tek göstergesi olarak kullanmamalısınız. Aynı zamanda, tüm analistler, mali direktörler ve yöneticiler için yatırım analizinde "sahip olunması gereken" göstergeler listesine aittir.