How to cancel an invoice. Seller's actions and buyer's actions. Invoices and other VAT documents Cancel an invoice in 1s 8.3

VAT reporting has already been submitted, but suddenly you found that one of the sales invoices was entered twice, and the paper invoice received from the supplier indicated a later date than you indicated when entering. How to remove from the infobase of the program "1C: Accounting 8" ed. 3.0 unnecessary invoices after the end of the reporting campaign? The answer is in the material of 1C experts.

If, after filing the declaration, the taxpayer discovers that some information was not reflected in the declaration (not fully reflected) or reveals errors, then in accordance with paragraph 1 of Article 81 of the Tax Code of the Russian Federation, he:

- is obliged to amend the tax return and submit an amended return if errors (distortions) have led to an underestimation of the tax;

- has the right to amend the declaration and submit an amended declaration, if the errors (distortions) did not lead to an underestimation of the amount of tax payable.

If the detected errors or distortions relate to previous tax (reporting) periods, then the tax base and the tax amount are recalculated for the period in which the indicated errors (distortions) were committed (paragraph 2, clause 1, article 54 of the Tax Code of the Russian Federation).

This is a general rule. But the taxpayer has the right to recalculate the tax base and the amount of tax liabilities and in the period of detection of errors.

This is possible in two cases:

- if it is impossible to determine the period of these errors (distortions);

- if such errors (distortions) led to the excessive payment of tax (paragraph 2, clause 1, article 54 of the Tax Code of the Russian Federation).

But when applying these rules, you need to consider the following features:

- the norm of paragraph 1 of Article 54 of the Tax Code of the Russian Federation does not apply to errors that are made due to incorrect reflection of tax deductions. This is due to the fact that the taxpayer reduces the amount of tax already calculated from the tax base for tax deductions (clause 1 of article 171 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated August 25, 2010 No. 03-07-11 / 363);

- recalculation of the tax base for VAT in the period of detection of an error made in previous tax periods is not provided for by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137 (hereinafter - Decree No. 1137).

Cancellation of sales book entry

If a correction is made to the issued invoice after the end of the tax period, the registration of the corrected invoice and the cancellation of the entry on the original invoice are made in an additional sheet of the sales book for the tax period in which the invoice was registered before the corrections were made (p 3, paragraph 11 of the Rules for keeping a sales book, approved by Decree No. 1137). And according to the Rules for keeping a book of purchases, approved. Decree No. 1137, upon receipt of a corrected invoice after the end of the current tax period, the cancellation of the invoice entry is made in an additional sheet of the purchase book for the tax period in which the invoice was registered before corrections were made to it (clause 4 of the Bookkeeping Rules purchases, approved by Decree No. 1137).

Despite the fact that these norms of Decree No. 1137 correlate the procedure for correcting the sales book and (or) purchase book only with making corrections to invoices, the use of additional sheets of the purchase book and (or) sales book is prescribed for any changes in the sales book and ( or) books of purchases of expired tax periods (letters of the Federal Tax Service of Russia dated 06.09.2006 No. ММ-6-03/ [email protected], dated April 30, 2015 No. BS-18-6/ [email protected]).

We will analyze the procedure for making such corrections in the 1C: Accounting 8 program (rev. 3.0) using an example.

Example

How to record a service rendered

The provision of an advertising service to the buyer of LLC "Clothes and Footwear" in the program "1C: Accounting 8" (rev. 3.0) is registered using the document Implementation(act, invoice) with the type of operation Services (act)(chapter Sales, subsection -> Sales, hyperlink Implementation (acts, invoices).

After posting the document, the following entries are entered in the accounting register:

Debit 62.01 Credit 90.01.1

Debit 90.03 Credit 68.02

- on the amount of VAT charged.

An entry with the type of movement is entered in the Sales VAT register Coming for the sales book, reflecting the accrual of VAT at a rate of 18%. A corresponding entry on the cost of the rendered advertising service is also made in the register Implementation of services.

You can create an invoice for the rendered advertising service by clicking on the button Issue an invoice at the bottom of the document Implementation(act, bill of lading). This automatically creates a document. invoice issued, and in the form of the base document, a hyperlink to the created invoice appears (Fig. 1).

Document Invoice issued(chapter Sales, subsection Sales, hyperlink Invoices issued), which can be opened via a hyperlink, all fields are filled in automatically based on the document data Implementation (act, invoice).

From 01/01/2015, taxpayers who are not intermediaries acting on their own behalf (forwarders, developers) do not keep a register of received and issued invoices, therefore, in the document Invoice issued in line "Sum:" it is indicated that the amounts for registration in the accounting journal (“of which in the journal:”) are equal to zero.

As a result of the document Invoice issued an entry is made in the register Invoice journal. Register entries Invoice journal are used to store the necessary information about the issued invoice.

With button Printing a Document accounting system Invoice issued You can view the invoice form and also print it.

Information from the sales book is reflected in section 9 of the VAT tax return.

Correction of accounting and tax accounting data

Accounting. According to clause 5 of the Accounting Regulations “Correction of errors in accounting and reporting” (PBU 22/2010)”, approved. By order of the Ministry of Finance of Russia dated June 28, 2010 No. 63n, an error in the reporting year identified before the end of this year is corrected by entries in the relevant accounting accounts in the month of the reporting year in which the error was discovered.

Tax accounting. If errors are found in the submitted tax return that do not lead to an understatement of the amount of tax payable, the taxpayer has the right, but is not obliged, to submit an updated tax return to the tax authority (clause 1, article 81 of the Tax Code of the Russian Federation).

In the example under consideration, a VAT-taxable operation for the provision of advertising services was erroneously recorded in accounting, therefore, the detected error led to an overestimation of the VAT tax base in Q3 2015 and, consequently, the amount of tax payable to the budget.

In accordance with paragraph 2 of clause 1 of Article 54 of the Tax Code of the Russian Federation, if errors (distortions) are found in the calculation of the tax base relating to previous tax (reporting) periods, in the current tax (reporting) period, the tax base and the amount of tax are recalculated for the period in which indicated errors (distortions) were committed. At the same time, if such errors (distortions) led to the excessive payment of tax, then the taxpayer has the right to recalculate the tax base and the amount of tax in the tax (reporting) period in which errors (distortions) were discovered (paragraph 2, clause 1, Art. 54 of the Tax Code of the Russian Federation). However, the rule that allows the recalculation of the tax base in the period when an error was discovered, i.e., in the fourth quarter of 2015, does not apply to VAT, since Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 does not provide for a mechanism for its implementation.

According to paragraph 3 and paragraph 2 of paragraph 11 of the Rules for maintaining the sales book, approved. Decree No. 1137, if it is necessary to cancel an entry in the sales book after the end of the current tax period, additional sheets of the sales book for the tax period in which the invoice was registered are used. Despite the fact that Resolution No. 1137 correlates this procedure with corrections to the sales book caused by corrections to invoices, the possibility of canceling erroneous registration entries is confirmed in the explanations of the Federal Tax Service of Russia (Letters of the Federal Tax Service of Russia dated 06.09.2006 No. MM-6-03 / [email protected], dated April 30, 2015 No. BS-18-6/ [email protected]).

The data of such sheets is used to make changes to the VAT declaration (clause 5 of the Rules for filling out an additional sheet of the sales book).

Correction of an error in the reflection in accounting and tax accounting of the fact of economic life that did not take place in the program is registered using the document Operation with the type of operation Document reversal(chapter Operations, subsection Accounting, hyperlink Operations entered manually).

The header of the document says:

- in field from- date of correction of the error;

- in field Reversible document- corresponding erroneous implementation document.

Bookmark Accounting and tax accounting the corresponding reversal accounting entries are reflected:

Debit 62.01 Credit 90.01.1

For the cost of services rendered;

Debit 90.03 Credit 68.02

- on the amount of VAT charged.

The corresponding reversal account will also be reflected in the register Service implementation(Fig. 3, document Operation).

A corresponding reversal entry is automatically made in the Sales VAT register with the following values:

- in the column Recording an additional sheet - "No";

- in the Adjustable period column - the value is missing;

- in the column Amount without VAT - "-80,000.00";

- in the VAT column - "-14,400.00".

Since the cancellation of the registration entry for an erroneously issued invoice should be made in an additional sheet of the sales book for the period of service provision, i.e. the third quarter of 2015, it is necessary to make an adjustment to the Sales VAT register entries:

- in the Record of an additional sheet column - change the value to Yes;

- in the Adjustable period column - indicate any date of the III quarter of 2015, for example, 09/30/2015.

After recording the document Operation, an entry will be made about the cancellation of the erroneously issued invoice in an additional sheet of the sales book for the III quarter of 2015 - see table. 2.

It should be noted that the erroneously issued invoice itself is not subject to cancellation (withdrawal, destruction). According to the Federal Tax Service of Russia, fixing the mechanism for canceling invoices is not advisable, since if an erroneously issued invoice is not registered in the sales book, then it is not accepted for accounting (letter of the Federal Tax Service of Russia dated April 30, 2015 No. BS-18-6 / [email protected]).

When making a decision to submit an amended tax return for VAT for the third quarter of 2015, it should be borne in mind that such an amended declaration will include the same sections as the primary declaration (clause 2 of the Procedure for filling out a tax return for VAT, approved by order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/ [email protected]).

At the same time, the title page of the VAT declaration will indicate the adjustment number “1” and the date of signature “10/27/2015”.

In section 3 of the revised tax return, line 010 will reflect the reduced tax base and the amount of calculated tax (Fig. 4).

In addition, an additional appendix 1 to section 9 will appear in the revised declaration, which will reflect information from an additional sheet of the sales book. Since there was no such information in the primary declaration, the Previously submitted information line will be marked as Irrelevant, which corresponds to the sign of relevance "0" and means that in the previously submitted declaration this information was not presented under section 9 (clause 48.2 of the Procedure for filling out a tax return under VAT).

Since no changes were made to the sales book itself, the information from section 9 can not be re-uploaded to the tax office, for which it is enough to check the Previously submitted information field in the Relevant field, which corresponds to the relevance sign "1" and means that the information provided by the taxpayer earlier to the tax authority, are relevant, reliable, are not subject to change and are not submitted to the tax authority (clause 47.2 of the Procedure for filling out a VAT tax return).

Cancellation of a purchase ledger entry

When corrections are made to the issued invoice after the end of the tax period, the registration of the corrected invoice and the cancellation of the entry on the original invoice are made in an additional sheet of the sales book for the tax period in which the invoice was registered before the corrections were made to it. 3, paragraph 11 of the Rules for keeping a sales book, approved by Decree No. 1137). Upon receipt of a corrected invoice after the end of the current tax period, the invoice entry is canceled in an additional sheet of the purchase book for the tax period in which the invoice was registered before corrections were made to it (clause 4 of the Rules for Maintaining the Purchase Book, approved by Decree No. 1137).

Despite the fact that these norms of Decree No. 1137 correlate the procedure for correcting the sales book and (or) the purchase book only with making corrections to invoices, the use of additional sheets of the purchase book and (or) the sales book is prescribed in relation to any changes in the sales book and ( or) books of purchases of expired tax periods (letters of the Federal Tax Service of Russia dated 06.09.2006 No. ММ-6-03/ [email protected], dated April 30, 2015 No. BS-18-6/ [email protected]).

The data of such additional sheets is used to make changes to the VAT tax return (clause 5 of the Rules for filling out an additional sheet of the sales book, clause 6 of the Rules for filling out an additional sheet of purchase books). At the same time, in addition to those sections that were previously submitted to the tax authority, the amended tax return includes, respectively, Appendix 1 to Section 8 and (or) Appendix 1 to Section 9 (clause 2 of the Procedure for filling out a VAT tax return, approved by order of the Federal Tax Service Russia dated October 29, 2014 No. ММВ-7-3/ [email protected]).

How to cancel the erroneous registration of the advance invoice in the sales book

1C experts

Having discovered in the current period an error of the previous period, as a result of which VAT was overpaid (for example, due to the erroneous recognition of the postpayment received from the buyer as an advance), the taxpayer can correct it: cancel the extra registration entry on the erroneous invoice in the sales book, recalculate the tax the VAT base in the period of detection of the error and submit an updated VAT return. The mechanism for correcting these errors is not provided for by Decree of the Government of the Russian Federation of December 26, 2011 N 1137, but in accordance with the explanations of the Federal Tax Service of Russia, erroneous registration entries can be canceled using additional sheets of the sales book. In the article, 1C experts, using the example of the "1C: Accounting 8" version 3.0 program, tell how to cancel an erroneous advance invoice.

The procedure for making corrections to the invoice after the end of the tax period

At the same time, the taxpayer has the right to recalculate the tax base and the amount of tax in the tax (reporting) period in which errors (distortions) were discovered, if (paragraph 3, clause 1, article 54 of the Tax Code of the Russian Federation):

it is impossible to determine the period of these errors (distortions);

such errors (distortions) led to the excessive payment of tax.

When applying these provisions to the calculation of VAT and the submission of tax returns on tax, the following features must be taken into account:

The data of such additional sheets is used to make changes to the VAT tax return (clause 5 of the Rules for filling out an additional sheet of the sales book). At the same time, in addition to those sections that were previously submitted to the tax authority, the amended tax return includes Appendix 1 to Section 9 (clause 2 of the Procedure for filling out a VAT tax return, approved by order of the Federal Tax Service of Russia dated 29.10.2014 N ММВ-7- 3/ [email protected]).

Cancellation of an erroneous advance invoice in "1C: Accounting 8" (rev. 3.0)

The procedure for correcting accounting and tax accounting data in the program "1C: Accounting 8" edition 3.0, starting from clarifying the purpose of the received funds, and up to the formation of an updated VAT return, we will consider the following example.

Example

On May 03, 2017, after submitting a VAT tax return for the 1st quarter of 2017, the organization TF-Mega LLC, which applies the general taxation system, discovered the fact of erroneous recognition of funds received from Clothing and Footwear LLC as an advance payment and, accordingly, erroneous registration issued advance invoice in the sales book for the 1st quarter of 2017.

The organization decided to make corrections in the accounting and tax accounting data, cancel the extra registration entry for the invoice in the sales book and submit an updated VAT tax return for the 1st quarter of 2017.

The sequence of operations is shown in table 1.

Receipt of funds from the buyer. Accounting for "advance" VAT

Receipt of advance payment on account of the forthcoming delivery of goods (operation 1.1 "Receipt of advance payment from the buyer") in the program is reflected using the Receipt to the current account document with the type of operation Payment from the buyer, which is formed:

on the basis of the document Invoice for payment to the buyer (section Sales - subsection Sales - document journal Invoices to buyers);

or by adding a new document to the Bank statements list (section Bank and cash desk - subsection Bank - document journal Bank statements).

As a result of posting the document Receipt to the current account, an accounting entry will be generated:

For the amount of advance payment received by the seller from the buyer.

Details (number and date of compilation) of the payment and settlement document (clause "h" clause 1 of the Filling Rules)

Name of the supplied goods (description of works, services), property rights (clause "a", clause 2 of the Filling Rules)

The amount of tax calculated on the basis of the tax rate determined in accordance with clause 4 of article 164 of the Tax Code of the Russian Federation (clause "h" clause 2 of the Filling Rules)

Received advance payment amount (clauses "and" clause 2 of the Filling Rules)

For the amount of VAT calculated from the received amount of prepayment from the buyer in the amount of 10,800.00 rubles. (70,800.00 rubles x 18/118).

The document Invoice issued will be registered in the sales VAT accumulation register. Based on the Sales VAT register entries, a sales book for the 1st quarter of 2017 is formed (section Sales - subsection VAT) (see Fig. 1).

Rice. 1. Sales book for the 1st quarter of 2017

Also, on the basis of the Issued Invoice document, an entry is made in the information register of the Invoice Accounting Journal.

Despite the fact that from 01.01.2015 taxpayers who are not intermediaries (forwarders, developers) do not keep a register of received and issued invoices, the records of the Register of invoices are used to store the necessary information about the issued invoice.

The invoice issued upon receipt of prepayment is registered in the sales book for the 1st quarter of 2017 (Fig. 1).

A VAT-taxable transaction related to the receipt of the prepayment amount is reflected in line 070 of Section 3 of the VAT tax return for the 1st quarter of 2017 (approved by order of the Federal Tax Service of Russia of October 29, 2014 N ММВ-7-3 / [email protected] in red. order of the Federal Tax Service of Russia dated December 20, 2016 N ММВ-7-3/ [email protected]) (operation 1.4 "Formation of the VAT return for the 1st quarter of 2017).

Information from the sales book is reflected in Section 9 of the VAT return.

Correction of accounting and tax accounting data

The funds received from the buyer on 03/26/2017 were erroneously recognized as advance payment under contract No. 25 dated 03/01/2017, and not payment for goods shipped to the buyer on 02/03/2017 under contract No. 15 dated 02/01/2017.

Due to the fact that the transaction subject to VAT on the calculation of tax on the received prepayment amount was erroneously reflected in the accounting, the detected error led to an overestimation of the tax base for VAT in the first quarter of 2017 and, consequently, the amount of tax payable to the budget.

Correction of an error in issuing an invoice and registering it in the sales book (operations: 2.2 "Reversal of VAT accrual on advances received", 2.3 "Cancellation of an entry on an erroneous invoice from the sales book") is registered in the program using the document Operation with the type document reversal operations (section Operations - subsection Accounting - hyperlink - Operations entered manually) (Fig. 3).

The header of the document says:

Rice. 3. Reversal of VAT accrual on advances received

The Accounting and tax accounting tab reflects the corresponding reversal accounting entry:

For the amount of VAT calculated from the received prepayment.

A corresponding reversal entry is automatically made in the Sales VAT register, indicating the following values (Fig. 4):

"Adjustable Period" | No value |

"Price without VAT" | |

Rice. 4. Cancellation of an entry on an erroneous invoice from the sales book before manual correction

Since the cancellation of the registration record for an erroneously issued invoice must be made in an additional sheet of the sales book of the period of receipt of funds, i.e. I quarter of 2017, it is necessary to make an adjustment in the records of the Sales VAT register (see Fig. 5):

"Additional sheet entry" | Change value to "Yes" |

"Adjustable Period" | Specify any date of the 1st quarter of 2017, for example, 03/31/2017 |

"Reversing additional sheet entry" | Change value to "Yes" |

Rice. 5. Cancellation of an entry on an erroneous invoice from the sales book after manual adjustment

Since, when calculating VAT on the received prepayment amount, an entry in the Sales VAT accumulation register was made in two lines, it is necessary to make an appropriate adjustment in each line.

After recording the document Operation, an entry about the cancellation of the erroneously issued advance invoice will be entered in an additional sheet of the sales book for the 1st quarter of 2017 (Fig. 6).

Rice. 6. Additional sheet of the sales book for the 1st quarter of 2017

It should be noted that the erroneously issued invoice itself is not subject to cancellation (withdrawal, destruction). According to the Federal Tax Service of Russia, fixing the mechanism for canceling invoices is inappropriate, because if the erroneously issued invoice is not registered in the sales book for Section 9, which will reflect information from the additional sheet of the sales book. Since there was no such information in the primary declaration, the Previously submitted information line will be marked as Not relevant, which corresponds to the relevance indicator "0" and means that this information was not provided in the previously submitted declaration under Section 9 (clause 48.2

Since no changes were made to the sales book itself, the information from Section 9 can not be re-uploaded to the tax office, for which it is enough to set a checkmark in the Previously submitted information field in the Relevant field, which corresponds to the relevance sign "1" and means that the information provided by the taxpayer earlier to the tax authority, are relevant, reliable, are not subject to change and are not submitted to the tax authority (clause 47.2 of the Procedure for filling out a VAT tax return).

The current version of the document you are interested in is available only in the commercial version of the GARANT system. You can purchase a document for 54 rubles or get full access to the GARANT system for free for 3 days.

If you are a user of the Internet version of the GARANT system, you can open this document right now or request it via the Hotline in the system.

We are starting a series of lessons on working with VAT in 1C: Accounting 8.3 (version 3.0).

Today we will consider the topic: "Corrected Invoice".

Most of the material will be designed for beginner accountants, but experienced ones will find something for themselves.

I remind you that this is a lesson, so you can safely repeat my actions in your database (preferably a copy or a training one).

So let's get started.

A bit of theory

Unlike a correction invoice, a corrected invoice is used to correct errors made when completing the original invoice.Corrections are made only in cases where filling errors are found, for example:

- typos,

- incorrect details,

- mixed up tax rates.

The number and date of the corrected invoice fully match the original document, but it additionally indicates the number and date of the correction.

Corrections are numbered within the primary invoice from 1 to infinity.

Consider possible situations with examples.

Vendor side fix

On January 1, 2016, we (NDS LLC) shipped 2 air conditioners to Buyer LLC at a price of 15,000 rubles each (including VAT).At the same time, we issued the primary invoice No. 1 dated 01/01/2016 to the buyer, in which we made a typo, indicating 3 air conditioners instead of two.

Issuing an initial invoice

Go to the section "Sales" item "Implementation (acts, invoices)":Create and fill out a new document "Sales (goods)":

We post it, and then issue an invoice (the button at the bottom of the document):

An error was discovered in the same tax period (at the seller)

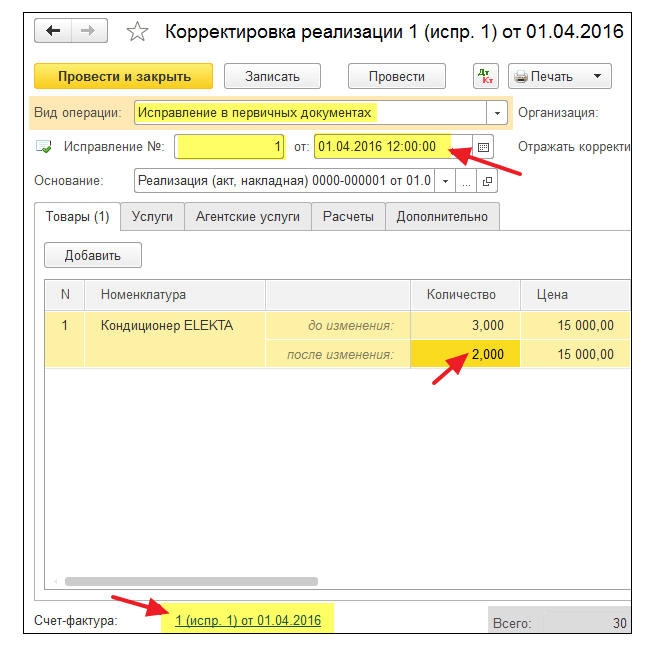

We discovered our mistake on January 10, when we issued the corrected invoice No. 1 (correction 1) dated 01/01/2016 (correction 01/10/2016) to the buyer.We issue a corrected invoice in the same tax period (from the seller)

Again we go to the "Sales" section, the item "Implementation (acts, invoices)":

Select the previously created implementation with the left mouse button, and then select the "Create based on" item (may be hidden in the "More" item) and then the "Implementation adjustment" item:

We fill in the adjustment of the implementation:

In doing so, pay attention to a few points:

- Type of operation "Correction in primary documents".

- Correction No. 1 dated 01/10/2016.

- Quantity 2.

We look at the sales book in the same tax period (from the seller)

We form the sales book for the 1st quarter:

And we see that the primary invoice is canceled (using the reversal method):

The corrected invoice was included in the sales book:

At the same time, the number and date of correction are also indicated there:

An error was found in a different tax period (from the seller)

We discovered our mistake on April 01, when we issued the corrected invoice No. 1 (correction 1) dated 01/01/2016 to the buyer (correction 04/01/2016).We issue a corrected invoice according to the same scheme (as above), only with the date 04/01/2016:

In this case (issuing a corrected invoice in another tax period), the correction is made through an additional sheet of the sales book of the 1st quarter.

Opening the sales book for the 1st quarter:

Click in it "Show settings":

Check the box "Generate additional sheets" for the current period:

We form the sales book and instead of the main section we indicate "Additional sheet for the 1st quarter of 2016":

Here is the cancellation of the primary invoice:

And here is the corrected invoice with the number and date of correction:

Buyer side fix

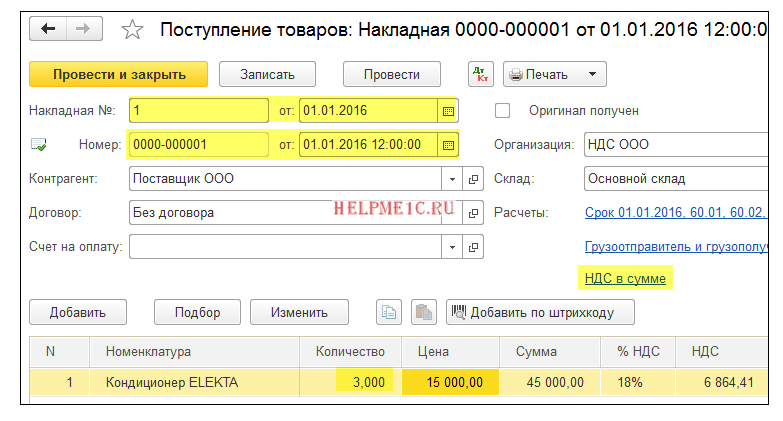

On January 1, 2016, we (NDS LLC) received 2 air conditioners from Supplier LLC at a price of 15,000 rubles each (including VAT).At the same time, we received the primary invoice No. 1 dated 01/01/2016, in which a typo was made (3 air conditioners were indicated instead of 2).

We enter the primary invoice

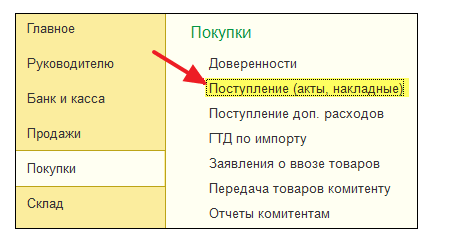

We go to the section "Purchases" item "Receipt (acts, invoices)":

Create and fill out a new document "Receipt (goods)":

We register the primary invoice at the bottom of the document:

The error was discovered in the same tax period (at the buyer)

The seller discovered his mistake on January 10, by issuing us (the buyer) a corrected invoice No. 1 (correction 1) dated 01/01/2016 (correction 01/10/2016).We enter the corrected invoice in the same tax period (from the buyer)

Again we go to the "Purchases" section, the item "Receipt (acts, invoices)":

Select the previously created receipt with the left mouse button, and then select the item "Create based on" (may be hidden in the "More" item) and then the item "Adjustment of receipt":

Fill in the income adjustment as follows:

On the "Goods" tab, indicate the correct quantity:

We post the document and register the corrected invoice:

We make an entry in the purchase book in the same tax period (at the buyer)

Go to the section "Operations" item "VAT Assistant":

Specify the period "1 quarter" and then open the formation of purchase book entries:

Click the "Fill Document" button:

The "Acquired Values" tab will automatically be filled in by our receipt, from the date of receipt of the invoice on 01/10/2016 (date of correction):

We post the document, and then form the book of purchases for the 1st quarter:

The primary invoice has been cancelled, a new (corrected) invoice has been submitted.

The error was found in another tax period (for the buyer)

The seller discovered his mistake on April 1, by issuing us (the buyer) corrected invoice No. 1 (correction 1) dated 01/01/2016 (correction 04/01/2016).We enter the corrected invoice according to the same scheme (as above), only with the date 04/01/2016:

In this case, the primary invoice is canceled through an additional sheet of the purchase book for the 1st quarter:

And the corrected invoice is entered into the shopping book for the 2nd quarter through entries in the shopping book.

To do this, open the "VAT Assistant" for the 2nd quarter:

And open the operation "Formation of purchase book entries":

In the form that opens, click the "Fill out the document" button:

The "Acquired Values" tab was automatically filled in with the corrected invoice dated 04/01/2016:

We post the document, and then form the book of purchases for the 2nd quarter:

The corrected invoice is entered in the book of purchases of the 2nd quarter.

For the 1st quarter of 15 years, the implementation of services was made, an invoice was accordingly issued, but this implementation was not accepted by the Customer, so it must be canceled, but simply deleting these documents from the accounting program is impossible, because. the serial numbering of invoices, acts will be violated .... How to do it right?

The invoice should be cancelled. To do this, fill out an additional sheet to the sales book for the period in which the error was made, and reflect in it the amount of shipment and tax on the erroneously issued invoice with a minus sign.

Adjust the tax base for VAT. Since the invoice issued was included in the total amount of sales for the tax period, then tax was overcharged from this amount. So, the organization formed an overpayment. Therefore, it is necessary to adjust the tax base and recalculate the tax. And, despite the fact that such an error led to an overpayment of VAT, in this situation it is necessary to submit an updated declaration to the tax office.

The rationale for this position is given below in the materials of the Glavbukh System

Situation:What should the seller organization do if it mistakenly issued two invoices for the same operation. This was discovered after filing a VAT return.

You will have to adjust the tax base for VAT, recalculate the tax, and also notify the buyer about the mistake.

Due to the fact that the invoice was issued repeatedly for the same operation, both the seller's VAT tax base and the buyer's tax deduction will be overestimated. Therefore, if you find such an error, you need to perform the following steps.

1. Void the reissued invoice in the sales book.

After all, it is on the basis of the sales book that the amount of VAT payable is determined (Section II of Appendix 5 to). To do this, fill out an additional sheet to the sales book for the period in which the error was made, and reflect in it the amount of shipment and tax on the erroneously issued invoice with a minus sign (paragraph 11 of section II of Appendix 5 to the Decree of the Government of the Russian Federation of December 26, 2011 city No. 1137).

2. Adjust the tax base for VAT for the period in which the error was made.

Since the reissued invoice was included in the total amount of sales for the tax period, then this amount was overcharged with tax. So, the organization formed an overpayment. Therefore, it is necessary to adjust the tax base and recalculate the tax. And despite the fact that such an error led to an overpayment of VAT, in this situation it is necessary to submit an updated declaration to the tax office. It is not possible to adjust the tax base in the current period. This is due to the fact that the general rules provided for the correction of errors in accordance with Article 81 and paragraph 1 of Article 54 of the Tax Code of the Russian Federation do not apply to VAT.*

Form an updated declaration on the basis of the corrected sales book, taking into account the completed additional sheet (clause 5 of section IV of Appendix 5 to Decree of the Government of the Russian Federation of December 26, 2011 No. 1137). The resulting tax overpayment can be set off or returned.

3. Notify the buyer of the error found.

It is clear that the buyer registered the erroneously issued invoice in the purchase book. And on the basis of the data of such a book, he forms the amount of tax accepted for deduction (Section II of Appendix 4 to Decree of the Government of the Russian Federation of December 26, 2011 No. 1137). By reflecting the extra invoice there, the buyer simply overestimated the amount of the deduction.

As a result, there is a arrears, because of which organizations can accrue penalties and fines.

Therefore, as soon as you discover that you have re-invoiced by mistake, be sure to inform the buyer about this - send him a notification. Based on such a document, he will be able to make changes to the purchase book and also submit an updated declaration.

Olga Tsibizova,

deputy director of the department

tax and customs tariff policy of the Ministry of Finance of Russia

- Download forms

The accountant decided to correct the data of accounting and tax accounting, as well as submit an updated tax return for VAT for the III quarter of 2015. How to reflect the rendered service in the accounting The provision of an advertising service to the buyer of OOO "Clothes and Footwear" in the program "1C: Accounting 8" (rev. 3.0) is registered using the document Implementation (act, invoice) with the type of operation Services (act) (section Sales, subsection -Sales, hyperlink Sales (acts, invoices) After posting the document, the following entries are entered into the accounting register: Debit 62.01 Credit 90.01.1 - for the cost of the advertising service rendered; Debit 90.03 Credit 68.02 - for the amount of VAT charged. The Sales VAT register is entered an entry with the movement type Receipt for the sales book, reflecting the accrual of VAT at the rate of 18%.

How to cancel an invoice?

But the taxpayer has the right to recalculate the tax base and the amount of tax liabilities and in the period of detection of errors. This is possible in two cases:

- if it is impossible to determine the period of these errors (distortions);

- if such errors (distortions) led to the excessive payment of tax (paragraph 2, clause 1, article 54 of the Tax Code of the Russian Federation).

But when applying these rules, you need to consider the following features:

- the norm of paragraph 1 of Article 54 of the Tax Code of the Russian Federation does not apply to errors that are made due to incorrect reflection of tax deductions. This is due to the fact that the taxpayer reduces the amount of tax already calculated from the tax base for tax deductions.

1 st.

Corrective or corrected invoice in 2018: how not to miss?

Decree No. 1137, upon receipt of a corrected invoice after the end of the current tax period, the cancellation of the invoice entry is made in an additional sheet of the purchase book for the tax period in which the invoice was registered before corrections were made to it (clause 4 of the Bookkeeping Rules purchases, approved by Decree No. 1137). Despite the fact that these norms of Decree No. 1137 correlate the procedure for correcting the sales book and (or) purchase book only with making corrections to invoices, the use of additional sheets of the purchase book and (or) sales book is prescribed for any changes in the sales book and ( or) books of purchases for expired tax periods (letters of the Federal Tax Service of Russia dated 06.09.2006 No. MM-6-03/, dated 30.04.2015 No. BS-18-6/). The data of such additional sheets are used to make changes to the VAT tax return (p.

How to register a corrected invoice for the previous period?

The difference between null and void invoices is the tax implications. So, if you register a zero invoice in the book of purchases or sales, there will be no consequences for the merchant; in the case of a canceled invoice, not everything is so simple ... Why cancel an invoice Everyone is prone to make mistakes, so errors in work sometimes occur.

An absent-minded accountant may issue an invoice to the wrong buyer or make a mistake in his details. In any case, errors need to be corrected, but this is not always done in the same way. For example, the original invoice contains information that does not correspond to reality, and this requires adjustments.

About cancellation of invoices (milenina n.v.)

Attention

Add to favoritesSend by email How do I cancel an invoice? This question arises when the invoice addressed to the counterparty was issued by mistake or needs to be replaced. About what needs to be done in such situations in order to avoid tax consequences and not let down your counterparties, we will tell in our article. Canceled and null invoice - what's the difference? Why cancel an invoice How to properly cancel an invoice to a seller Cancellation of an invoice by a buyer Summary Canceled and null invoices - what's the difference? A zero invoice can be issued by merchants, if they do not apply VAT (for example, "simplified"), at the request of the counterparty.

At the same time, the Tax Code does not provide for the obligation to issue zero invoices for them. Read more about VAT under the simplified tax system in the material "VAT under the simplified tax system: in what cases to pay and how to take into account tax in 2017-2018?".

April 12, 2018invoices "from the past": disputes over timing

If an erroneous invoice were discovered after the end of the third quarter, the accountant of Romashka LLC would have to draw up an additional sheet of the sales book and register the erroneously issued invoice (with a minus sign) in it, then reflect the invoice to LLC “ Spikelet" for the same amount (clause 3 of the rules for filling out the sales book). At the same time, the total sales amounts of Romashka LLC would remain unchanged and there would be no need for an updated declaration (clause 1, article 81 of the Tax Code of the Russian Federation, clause 2 of Appendix 2 to the order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3 / ). However, in the situation under consideration, the data provided by Romashka LLC in Appendix 9 to the VAT return for the 3rd quarter will be incorrect and the tax authorities, if an error is found, will require clarification (p.

3 art. 88 of the Tax Code of the Russian Federation).

Deleting an erroneous receipt document in "1s: accounting 8"

Info

Despite the fact that these norms of Decree No. 1137 correlate the procedure for correcting the sales book and (or) the purchase book only with making corrections to invoices, the use of additional sheets of the purchase book and (or) the sales book is prescribed in relation to any changes in the sales book and ( or) books of purchases for expired tax periods (letters of the Federal Tax Service of Russia dated 06.09.2006 No. MM-6-03/, dated 30.04.2015 No. BS-18-6/). The data of such additional sheets is used to make changes to the VAT tax return (clause 5 of the Rules for filling out an additional sheet of the sales book, clause 6 of the Rules for filling out an additional sheet of purchase books). At the same time, in addition to those sections that were previously submitted to the tax authority, the amended tax return shall include, respectively, Appendix 1 to Section 8 and (or) Appendix 1 to Section 9 (clause 3).

To do this, the program should generate two documents Operation relating to different periods:

- dated September 2015 - only for adjusting tax accounting data for income tax;

- with the Reversal type of the document dated February 2016 - to adjust accounting data and tax accounting data for VAT.

When creating a manually entered Transaction in September 2015 (Fig. 5), two entries must be entered into special resources for tax accounting purposes: STORNO Amount NU Dt 90.02.1 Amount NU Kt 76.K

- the amount of erroneously reflected direct costs;

Amount NU Dt 90.09 Amount NU Kt 99.01.1

- by the amount of the financial result obtained as a result of corrections made to tax accounting.

In this case, permanent and temporary differences are not reflected. Rice. 2.

The question immediately arises: how to cancel an invoice and are there other ways to correct it? Cases where you can do without cancellation, although the original invoice requires adjustments, are listed in paragraph 5.2 of Art. 169 of the Tax Code of the Russian Federation. This happens, for example, when the cost of goods (works, services) changes due to the adjustment of their price or quantity. This does not raise questions about how to cancel the invoice, since the change in the tax obligations of the buyer and seller will be reflected in the books of purchases and sales based on the adjustment invoice.

It is important to remember that it does not replace the original invoice, but only makes adjustments to it, that is, the existence of an adjustment invoice is possible only together with the original one.

III quarter of 2015, it is necessary to make an adjustment in the VAT register entries Sales:

- in the Record of an additional sheet column - change the value to Yes;

- in the Adjustable period column - indicate any date of the III quarter of 2015, for example, 09/30/2015.

After recording the document Operation, an entry will be made about the cancellation of the erroneously issued invoice in an additional sheet of the sales book for the III quarter of 2015 - see table. 2. Table 2 It should be noted that the erroneously issued invoice itself is not subject to cancellation (withdrawal, destruction). According to the Federal Tax Service of Russia, fixing the mechanism for canceling invoices is not advisable, since if an erroneously issued invoice is not registered in the sales book, then it is not accepted for accounting (letter of the Federal Tax Service of Russia dated April 30, 2015 No. BS-18-6 /