Absolute liquidity ratio formula for the balance sheet. Absolute liquidity ratio and normative value

Liquidity - ease of sale, sale, transformation of material or other values into cash to cover current financial obligations.

Liquidity ratios - financial indicators, calculated on the basis of the company's statements (balance sheet of the company - form No. 1) to determine the company's ability to repay current debt at the expense of existing current (current) assets. The meaning of these indicators is to compare the value of the current debts of the enterprise and its working capital, which should ensure the repayment of these debts.

Consider the main liquidity ratios and formulas for their calculation:

Calculation of liquidity ratios allows you to analyze the liquidity of the enterprise, i.e. analysis of the possibility for the enterprise to cover all its financial obligations.

Note that the assets of the enterprise are reflected in the balance sheet and have different liquidity. Let's rank them in descending order, depending on the degree of their liquidity:

- cash in the accounts and cash desks of the enterprise;

- bank bills, government securities;

- current receivables, loans issued, corporate securities (shares of enterprises listed on the stock exchange, bills of exchange);

- stocks of goods and raw materials in warehouses;

- cars and equipment;

- buildings and constructions;

- Construction in progress.

Current liquidity ratio

Current liquidity ratio or Coverage ratio or General liquidity ratio - a financial ratio equal to the ratio of current (current) assets to short-term liabilities (current liabilities). The source of data is the company's balance sheet (Form No. 1). The coefficient is calculated by the formula:

Current liquidity ratio \u003d Current assets, excluding long-term accounts receivable/ Short-term liabilitiesKtl = (p. 290 - p. 230) / p. 690 or

Ktl = p. 290 / (p. 610 + p. 620 + p. 660)Ktl = line 1200 / (line 1520 + line 1510 + line 1550)

The ratio reflects the company's ability to repay current (short-term) liabilities at the expense of current assets only. The higher the indicator, the better the solvency of the enterprise. Current liquidity ratio characterize the solvency of the enterprise not only on this moment but also in case of emergency.

The normal value of the coefficient is from 1.5 to 2.5, depending on the industry. Both low and high ratios are unfavorable. A value below 1 indicates a high financial risk associated with the fact that the company is not able to consistently pay current bills. A value greater than 3 may indicate an irrational capital structure. But at the same time, it must be taken into account that, depending on the field of activity, the structure and quality of assets, etc., the value of the coefficient can vary greatly.

It should be noted that this ratio does not always give a complete picture. Typically, firms with low inventories and easily obtainable bills of exchange can easily operate at a lower ratio than firms with large inventories and sales of goods on credit.

Another way to check the sufficiency of current assets is to calculate urgent liquidity. Banks, suppliers, shareholders are interested in this indicator, since the company may face circumstances in which it will immediately have to pay some unforeseen expenses. So she'll need all her cash, securities, receivables and other means of payment, ie, part of the assets that can be turned into cash.

Quick (urgent) liquidity ratio

The ratio characterizes the company's ability to repay current (short-term) liabilities at the expense of current assets. It is similar to the current liquidity ratio, but differs from it in that the working capital used for its calculation includes only highly - and medium liquid current assets (money in operating accounts, stock of liquid materials and raw materials, goods and finished products, receivables with a short maturity).

Such assets do not include work in progress, as well as inventories of special components, materials and semi-finished products. The source of data is the company's balance sheet in the same way as for current liquidity, but inventories are not taken into account as assets, since if they are forced to be sold, losses will be maximum among all current assets:

Quick liquidity ratio = (Cash + Short-term financial investments + Short-term receivables) / Current liabilities

Quick liquidity ratio = (Current assets - Stocks) / Short-term liabilities

Kbl = (p. 240 + p. 250 + p. 260) / (p. 610 + p. 620 + p. 660)

Kbl = (p. 1230 + p. 1240 + p. 1250) / (p. 1520 + p. 1510 + p. 1550)

This is one of the important financial ratios, which shows what part of the company's short-term liabilities can be immediately repaid from the funds in various accounts, in short-term securities, as well as proceeds from settlements with debtors. The higher the indicator, the better the solvency of the enterprise. The normal value of the coefficient is more than 0.8 (some analysts consider the optimal value of the coefficient 0.6-1.0), which means that cash and future receipts from current activities should cover the current debts of the organization.

To increase the level of urgent liquidity, organizations should take measures aimed at increasing their own working capital and attracting long-term loans and borrowings. On the other hand, a value of more than 3 may indicate an irrational capital structure, this may be due to the slow turnover of funds invested in inventories, the growth of receivables.

In this regard, the coefficient can serve as a litmus test of current solvency absolute liquidity, which must be greater than 0.2. The absolute liquidity ratio shows what part short-term debt the organization can repay in the near future at the expense of the most liquid assets ( Money and short-term securities).

Absolute liquidity ratio

A financial ratio equal to the ratio of cash and short-term financial investments to short-term liabilities (current liabilities). The data source is the company's balance sheet in the same way as for current liquidity, but only cash and cash equivalents are taken into account as assets, the calculation formula is as follows:

Absolute liquidity ratio = (Cash + Short-term financial investments) / Current liabilities

Cab = (p. 250 + p. 260) / (p. 610 + p. 620 + p. 660)

Cab = (p. 1240 + p. 1250) / (p. 1520 + p. 1510 + p. 1550)

A coefficient value of more than 0.2 is considered normal. The higher the indicator, the better the solvency of the enterprise. On the other side, high rate may indicate an irrational capital structure, an overly high proportion of non-performing assets in the form of cash and funds in accounts.

In other words, if the balance of funds is maintained at the level of the reporting date (mainly by ensuring a uniform receipt of payments from counterparties), short-term debt for reporting date can be repaid in five days. The above regulatory limitation is applied in foreign practice financial analysis. With this exact justification why to maintain normal level liquidity of Russian organizations, the amount of cash should cover 20% of current liabilities, is not available.

Net working capital

Net working capital is necessary to maintain the financial stability of the enterprise. Net working capital is defined as the difference between current assets and short-term liabilities, including short-term borrowed funds, accounts payable, liabilities equated to it. Net working capital is a part of working capital formed from own working capital and long-term borrowed capital, including quasi-own capital, borrowed funds and other long-term liabilities. The formula for calculating net settlement capital is:

Net Working Capital = Current Assets - Current Liabilities

Chob = p. 290 - p. 690

Chob = p. 1200 - p. 1500

Net working capital is necessary to maintain the financial stability of the enterprise, since the excess of working capital over short-term liabilities means that the enterprise can not only pay off its short-term liabilities, but also has reserves for expanding activities. Net working capital must be above zero.

The lack of working capital indicates the inability of the company to repay short-term liabilities in a timely manner. A significant excess of net working capital over the optimal need indicates the irrational use of enterprise resources.

Formulas for calculating liquidity ratios in accordance with international standards described in

Absolute liquidity ratio(English analogue of Cash Ratio) - the ratio of the most liquid part of assets and current (short-term) liabilities. The most liquid part of assets includes cash and cash equivalents. The indicator shows the share of the company's current liabilities that can be repaid immediately. This indicator is for group of liquidity indicators.

Standard value

The normative value is from 0.1 to 0.2. A lower indicator indicates that the company will not be able to repay debts on time if payments fall due soon. A value above the norm can also indicate problems in the company and indicate an ineffective management strategy. financial resources. Cash, unlike other assets, does not take part in the production and sales process, they do not generate income for the company. Therefore, a too high indicator indicates that a significant part of the capital is diverted to the formation of unproductive assets.

Directions for solving the problem of finding an indicator outside the normative limits

If the value of the indicator is below the norm, then the company may borrow money, implement some of the extra assets to increase the amount of the most liquid assets. If the value of the indicator is higher than the norm, then the company can invest part of the money(above the norm) in production and marketing activities, in financial investment etc.

The formula for calculating the coefficient:

Absolute liquidity ratio = Cash and cash equivalents / Current liabilities

Notes and corrections

Cash is a means that all participants in the financial process agree to exchange when making financial transactions. For cash to be classified as current assets, it is necessary that there are no restrictions on their storage and use. This situation is possible, for example, in the case of a court decision to seize funds. If there are such restrictions, then it is necessary to adjust the indicator of cash and cash equivalents, which is used in the calculation of the indicator.

Companies often display restricted cash as cash and cash equivalents on the balance sheet. In this case, information on restrictions can be found in the notes to financial reporting. In addition to reducing the amount of cash and cash equivalents by the amount of the limited part, it is also necessary to adjust the value of current liabilities and subtract those associated with the limit.

An example of calculating the absolute liquidity ratio:

JSC "WebInnovation-plus"

Unit of measurement: thousand rubles

Absolute liquidity ratio (2016) = 75/242 = 0.31

Absolute liquidity ratio (2015) = 46/236 = 0.2

The data obtained show that in 2015 each ruble of current liabilities accounted for about 0.2 rubles of cash and their equivalents. Thus, JSC "WebInnovation-plus" could meet its obligations in 2015. In 2016, the situation changed and the coefficient value was 0.31.

To reduce this value, it is advisable to allocate part of the funds, for example, to the purchase of bonds of other enterprises. This will allow you to receive additional interest income and at the same time remain liquid. Optimal size such an investment will be 75 - (242 * 0.2) \u003d 26.6 thousand rubles. Accordingly, (75 - 26.6) = 48.4 thousand rubles. - this is the amount of cash and equivalents at which absolute liquidity will be within the regulatory limits with a constant value of the amount of current liabilities.

Using the absolute liquidity ratio, it is determined what part of immediate debts can be repaid at the expense of cash and their analogues (securities, bank deposits etc.). That is, through highly liquid assets.

The absolute liquidity ratio, along with other liquidity indicators, is of interest not only to the management of the organization, but also to external subjects of analysis. So, this ratio is important for investors, quick liquidity - for banks; and absolute - to suppliers of raw materials and materials.

Definition and formula in Excel

Absolute liquidity shows the short-term solvency of the organization: whether the company is able to pay off its obligations (with counterparties-suppliers) through the most liquid assets (money and cash equivalents). The coefficient is calculated as the ratio financial resources to current liabilities.

The standard calculation formula looks like this:

Cubs. = (cash + short-term cash investments) / Current responsibility

Cubs. = highly liquid assets / (most current liabilities + medium-term liabilities)

The data for calculating the indicator are taken from balance sheet. Consider an example in Excel.

We circled the lines that are needed to calculate the absolute liquidity ratio. Balance formula:

Cubs. = (p. 1240 + p. 1250) / (p. 1520 + p. 1510).

Calculation example in Excel:

Just substitute the values of the corresponding cells (in the form of links) into the formula.

Absolute liquidity ratio and normative value

Accepted in foreign practice normative value coefficient – > 0.2. The essence of the restriction: every day the company must repay at least 20% of current liabilities. The practice of financial analysis in Russian companies adheres to the same principles. However, there is no justification for such an approach.

The structure of short-term debt in Russian practice is heterogeneous. Repayment terms vary considerably. Therefore, the figure 0.2 should be considered insufficient. For many enterprises, the coefficient rate is in the range of 0.2-0.5.

If the absolute liquidity ratio is below the norm:

- the enterprise cannot immediately settle accounts with suppliers using all types of funds (including proceeds from the sale of securities);

- economists need to further analyze solvency.

A large increase in the absolute liquidity ratio shows:

- too much non-performing assets in the form of cash on hand and on bank accounts;

- further analysis of the use of capital is needed.

Thus, the higher the indicator, the higher the liquidity of the company. But excessively high values indicate the irrational use of funds: the enterprise has an impressive amount of finance that is not “invested in the business”.

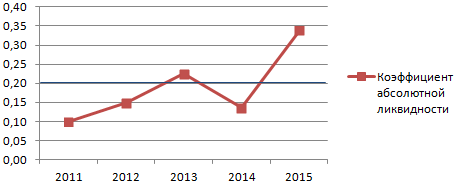

Let's go back to our example.

The values of absolute liquidity in 2013 and 2015 are within the normal range. And in 2014, the company experienced difficulties with the repayment of short-term liabilities.

Let us illustrate the dynamics of the indicator and for good example display on the chart:

To make a complete analysis of the solvency of the enterprise, all indicators of the liquid current assets of the organization are calculated. This ratio is used to calculate the share of short-term liabilities that can be repaid immediately. The example shows that the value for the period 2011-2015. increased by 0.24. In 2011, 2012 and 2014 the company experienced solvency difficulties. But the situation has normalized - the company is able to fulfill its current obligations by 34%.

Liquidity from an economic point of view shows the extent to which legal entity resources are able to move into the category of cash. The use of the absolute liquidity ratio makes it possible to understand what percentage of the obligations assumed by the enterprise can be repaid using available assets.

When assessing the level of solvency, organizations resort to the calculation and subsequent analysis of liquidity ratios. Thanks to the current indicator, you can understand in what proportion the existing assets transferred to monetary units, with every ruble of short-term debt.

Dear readers! The article talks about typical solutions legal issues but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

Quick liquidity indicates the ability of the company to carry out immediate repayment of debt with the help of money, investments, as well as debts owed to the company.

Absolute liquidity makes it possible to identify the company's ability to service current liabilities solely at the expense of available funds at a particular moment.

The meaning of the concept

The concept of liquidity is applied in relation to the process of selling an owned legal entity. the person of the property.

Depending on how fast this property can be sold, it is divided into:

When taking into account the first three types of property included in the category of current assets, indicators are calculated by which it is possible to determine to what extent a legal entity is able to pay short-term debts on it. The characteristics obtained during the calculation are called liquidity ratios.

Standard value

The absolute liquidity ratio is less in demand than those that serve to determine quick and current liquidity, so a clear norm has not been established for it.

In most cases, an indicator is considered normal, the value of which is 0.2 or higher. At the same time, if this ratio is excessively high, this indicates that the company is holding too much free cash that could be used for further business development.

In practice, the normal value of the coefficient can vary greatly, as it largely depends on the industry in which the enterprise operates. In order to calculate the acceptable level, one should take into account the speed with which current assets and liabilities are turned over.

In the case of assets turnover for a shorter period compared to the period of potential deferral of liabilities, solvency will be considered normal.

Basic moments

Working with data

To make calculations and determine the liquidity ratio, it is traditionally used as a source of initial data financial statements. On the balance sheet of the company, you can easily perform all the desired calculations by finding the ratio of the sum of codes 1240 and 1250 to the sum of codes 1510, 1520 and 1550.

The most liquid assets are in the numerator. Line 1240 reflects the amount of financial investments, the term of which is less than a year, while the monetary expression is not taken into account. This includes debt securities, funds used as statutory contributions in other organizations, loans issued to some companies, other investments.

Code 1250 reflects cash and cash equivalents. This category includes money available directly at the cash desk and in accounts, deposits, transfers expected to be received, securities with a high level of liquidity.

The absolute liquidity ratio is expressed as the ratio of highly liquid assets to term and short-term liabilities. The denominator indicates borrowed funds available to other debtors, as well as other obligations.

Relationship with solvency

To obtain the most accurate and reliable information regarding the solvency of the company, a detailed internal analysis, based on data obtained through accounting.

Previously, discount standards, which were practically not used in 2020 in determining liquidity, were especially popular. The basis for this system was the average estimates of the liquidity of all items in the balance sheet, as well as the development of discount rates that allow redistribution of balance sheet items between other groups.

For example, quick assets accounted for 80 percent of existing receivables, 70 percent of manufactured goods, and half of inventories with work in progress. Everything else was classified as a slow-moving asset.

By analogy, there was a redistribution of accounts payable, that is, a certain proportion of long-term debt was considered short-term, as well as vice versa.

Solvency also depends on the structure of capital, including the main one. In particular, with high demand and high exchange quotations for shares with promissory notes and other securities sale is possible with minor losses. In this regard, they turn into a more liquid commodity than some products.

In such a situation, it is not necessary for an enterprise to have a high liquidity ratio, since the fixed capital can be stabilized by selling part of the fixed capital.

How to calculate

The calculation of the coefficient is quite simple to make, based on the following postulates:

- it represents the ratio of highly liquid assets to current liabilities;

- It can also be viewed as the ratio of available money to current financial investments and obligations;

- in balance terms, this is the ratio of the sum of the 250th and 260th lines to the sum of the 610th, 620th and 660th lines.

The amount received as a result of the calculation will clearly reflect the real capabilities of the organization. O financial stability companies can be said with a coefficient in the region of 0.2-0.25, since this means that it is able to painlessly allocate a fourth to a fifth of its own funds to pay off current debt.

Absolute Liquidity Ratio Formula

The following formula is used to calculate the absolute liquidity ratio:

K = Highly liquid current assets / Short-term liabilities

The category of highly liquid current assets is usually classified as cash available at the box office and in bank accounts, as well as short-term financial investments. The category of current liabilities includes loans that must be repaid in the coming year, unscheduled requirements, as well as other obligations of a current nature.

Existing species

Current

It is determined by finding the ratio of current (called current) assets to current liabilities (short-term liabilities). The ratio calculated in this way allows us to conclude how the company is able to repay short-term obligations, using exclusively current assets for this.

The higher it gets this indicator, the better solvency the company has, and not only immediately, but also in the event of any unforeseen circumstances. Depending on the industry in which the enterprise operates, a coefficient ranging from 1.5 to 2.5 is considered normative.

Too low a coefficient that does not reach 1 indicates significant financial risks, as the company cannot ensure stable payment of current bills. At the same time, a coefficient exceeding 3 is also unfavorable, since it is a sign of the irrational use of equity capital.

Urgent

Shows how the company is able to cope with the repayment of short-term obligations, using only current assets. Unlike current liquidity, in this case only current assets of medium and high liquidity are taken into account.

Thereby financial ratio you can find out what part of the company's short-term liabilities can be immediately liquidated through the use of funds available in various accounts, short-term securities, repaid receivables.

The growth of this indicator (0.6-1.0 is considered normal) indicates that the solvency of the enterprise is increasing and there will be no problems with covering current debts. But the coefficient should also not be excessively high, since in this case it will be clear that available funds are used irrationally, while they could be directed to the development of the enterprise.

Using the net working capital ratio, an assessment is made of how the company is able to maintain its financial stability. It is defined as the difference between assets in circulation and liabilities of a short-term nature, which also includes borrowed funds taken for a short period, available accounts payable, as well as the obligations that are equated to it.

It is customary to characterize net working capital as part of working capital, which is formed by own working and long-term borrowed capital, including the so-called quasi-ownership capital, borrowed funds, and other long-term liabilities.

The need for net working capital is determined by the requirement to maintain the financial stability of the firm. If her working capital exceed short-term liabilities, this is an example of a company not only being able to meet its short-term liabilities, but also has sufficient reserves to expand its activities.

The value of working capital must always be above zero.

Value Analysis

Determining the solvency of the enterprise, it is advisable to consider the full capital structure, taking into account the main one. In the event that a company has significant assets, that is, shares with bills and other securities, and at the same time they have good quotes on the stock exchange, then when paying off debts, it makes sense to sell them as guaranteeing high liquidity.