Ministry of Finance order 66

In order to improve legal regulation in the field of accounting and financial reporting of organizations (with the exception of credit institutions, state (municipal) institutions) and in accordance with the Regulation on the Ministry of Finance of the Russian Federation, approved by Resolution of the Government of the Russian Federation No. 329 (Collected Legislation of the Russian Federation, 2004, N 31, Art. 3258; N 49, Art. 4908; 2005, N 23, Art. 2270; N 52, Art. 5755; 2006, N 32, Art. 3569; N 47 , art. 4900; 2007, N 23, art.

Ministry of Finance approved new forms of financial statements

2801; N 45, Art. 5491; 2008, N 5, Art. 411; 46, Art. 5337; 2009, N 3, Art. 378; No. 6, art. 738; N 8, Art. 973; 11, Art. 1312; No. 26, Art. 3212; 31, Art. 3954; 2010, N 5, Art. 531; N 9, Art. 967; 11, Art. 1224), I order:

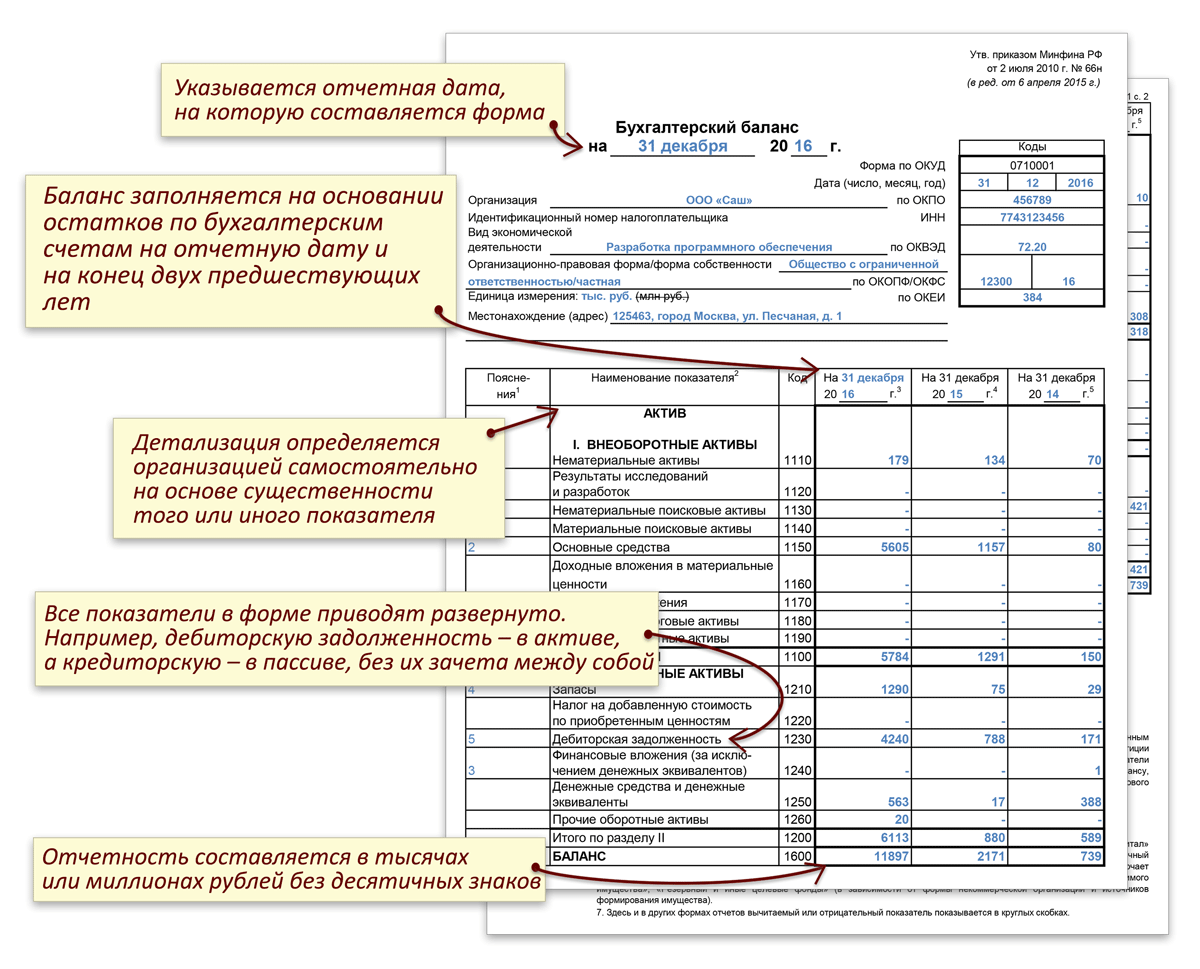

1. To approve the forms of the balance sheet and the statement of financial results in accordance with Appendix No. 1 to this Order.

2. To approve the following forms of appendices to the balance sheet and the statement of financial results in accordance with Appendix No. 2 to this Order:

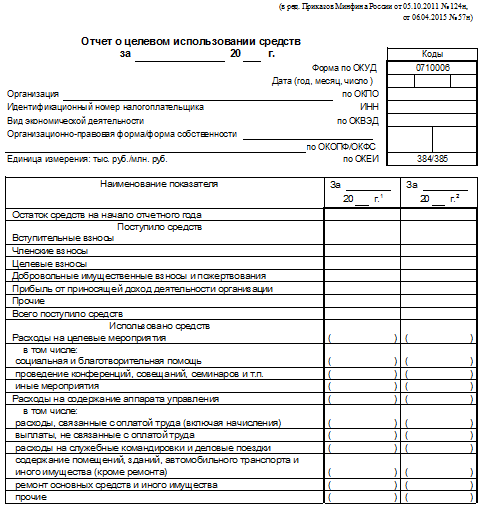

c) the form of the report on the targeted use of funds.

4. Establish that other appendices to the balance sheet and the statement of financial results (hereinafter - explanations):

If the financial statements of certain categories of organizations that are entitled to use simplified accounting methods, including simplified accounting (financial) statements, include aggregated indicators that include several indicators (without their detailing), the line code is indicated by the indicator having the largest specific weight as part of the enlarged indicator.

6. Establish that organizations that are entitled to use simplified accounting methods, including simplified accounting (financial) statements, generate financial statements according to the following simplified system:

a) the balance sheet, the statement of financial results, the report on the targeted use of funds include indicators only for groups of articles (without detailing indicators for articles);

b) in the appendices to the balance sheet, the statement of financial results, the statement on the targeted use of funds, only the most important information is provided, without which it is impossible to assess the financial position of the organization or the financial results of its activities.

Organizations that are entitled to use simplified methods of accounting, including simplified accounting (financial) statements, may form the submitted financial statements in accordance with paragraphs 1-4 of this Order.

6.1. To approve the simplified forms of the balance sheet of the statement of financial results, the report on the targeted use of funds for organizations that are entitled to use simplified methods of accounting, including simplified accounting (financial) statements, in accordance with Appendix No. 5 to this order.

Reference books and standards / Normative acts / Orders

MINISTRY OF FINANCE OF THE RUSSIAN FEDERATION

ORDER N 66n

ABOUT THE FORMS OF ACCOUNTING REPORTING OF ORGANIZATIONS

In order to improve legal regulation in the field of accounting and financial reporting of organizations (with the exception of credit institutions, state (municipal) institutions) and in accordance with the Regulation on the Ministry of Finance of the Russian Federation, approved by Resolution of the Government of the Russian Federation No. 329 (Collected Legislation of the Russian Federation, 2004, N 31, Art. 3258; N 49, Art. 4908; 2005, N 23, Art.

Error 404

2270; No. 52, Art. 5755; 2006, N 32, Art. 3569; 47, Art. 4900; 2007, N 23, Art. 2801; N 45, Art. 5491; 2008, N 5, Art. 411; 46, Art. 5337; 2009, N 3, Art. 378; No. 6, art. 738; N 8, Art. 973; 11, Art. 1312; No. 26, Art. 3212; 31, Art. 3954; 2010, N 5, Art. 531; N 9, Art. 967; 11, Art. 1224), I order:

a) the form of the statement of changes in equity;

b) the form of the statement of cash flows;

3. Establish that organizations independently determine the details of indicators according to the articles of reports provided for in paragraphs 1 and 2 of this Order.

a) are made out in tabular and (or) text form;

5. Establish that in the financial statements submitted to the state statistics bodies and other executive bodies, after the column, a column is given. The column indicates the codes of indicators in accordance with Appendix No. 4 to this Order.

7. To establish that this Order comes into force starting from the annual financial statements for 2011.

Deputy Prime Minister

Russian Federation - Minister of Finance

Russian Federation

A. L. KUDRIN

Comments on the material: (no comments yet)

Note to the document

In accordance with paragraph 7, this document comes into force starting from the annual financial statements for 2011.

Document's name

Order of the Ministry of Finance of the Russian Federation of 07/02/2010 N 66n

"On the forms of financial statements of organizations"

(Registered in the Ministry of Justice of the Russian Federation on 02.08.2010 N 18023)

MINISTRY OF FINANCE OF THE RUSSIAN FEDERATION

ABOUT THE FORMS OF ACCOUNTING REPORTING OF ORGANIZATIONS

In order to improve legal regulation in the field of accounting and financial reporting of organizations (with the exception of credit institutions, state (municipal) institutions) and in accordance with the Regulation on the Ministry of Finance of the Russian Federation, approved by Resolution of the Government of the Russian Federation No. 329 (Collected Legislation of the Russian Federation, 2004, N 31, Art. 3258; N 49, Art. 4908; 2005, N 23, Art. 2270; N 52, Art. 5755; 2006, N 32, Art. 3569; N 47 4900; 2007, N 23, Art.2801; N 45, Art.5491; 2008, N 5, Art.411; N 46, Art.5337; 2009, N 3, Art.378; N 6, Art. 738; N 8, Art. 973; N 11, Art. 1312; N 26, Art. 3212; N 31, Art. 3954; 2010, N 5, Art. 531; N 9, Art. 967; N 11, Art. 1224), I order:

1. To approve the forms of the balance sheet and the profit and loss statement in accordance with Appendix No. 1 to this Order.

2. To approve the following forms of appendices to the balance sheet and the income statement in accordance with Appendix No. 2 to this Order:

a) the form of the statement of changes in equity;

b) the form of the statement of cash flows;

c) the form of a report on the targeted use of the funds received, included in the accounting statements of public organizations (associations) that do not carry out entrepreneurial activities and do not have, apart from the retired property, sales of goods (works, services).

Order of the Ministry of Finance of the Russian Federation of 07/02/2010 N 66n

Establish that organizations independently determine the details of indicators according to articles of reports provided for in paragraphs 1 and 2 of this Order.

4. Establish that other appendices to the balance sheet and profit and loss statement (hereinafter - explanations):

a) are made out in tabular and (or) text form;

Recommend that non-profit organizations, with the exception of public organizations (associations) that do not engage in entrepreneurial activity and do not have sales of goods (works, services), except for retired property, use the report form on the targeted use of the funds received when forming appropriate explanations.

5. Establish that in the financial statements submitted to the state statistics bodies and other executive authorities, after the column "Name of the indicator" is the column "Code". The column "Code" indicates the codes of indicators in accordance with Appendix No. 4 to this Order.

6. Establish that organizations - small businesses generate financial statements according to the following simplified system:

a) the balance sheet and profit and loss statement include indicators only for groups of items (without detailing indicators by items);

b) in the appendices to the balance sheet and the profit and loss statement, only the most important information is provided, without knowing which it is impossible to assess the financial position of the organization or the financial results of its activities.

Organizations - small businesses have the right to form the submitted financial statements in accordance with paragraphs 1 - 4 of this Order.

7. To establish that this Order comes into force starting from the annual financial statements for 2011.

Deputy

Prime Minister

Russian Federation -

Minister of Finance

Russian Federation

A. L. KUDRIN

Information provided by the company "ConsultantPlus"

ORDER No. 66n On the forms of financial statements of organizations

About the forms of financial statements of organizations

Balance sheet form approved by the Ministry of Finance of Russia

Ministry of Finance. The form of the balance sheet was approved by order of the Ministry of Finance of Russia dated July 2, 2010 The form of the balance sheet netto, approved by the Ministry of Finance of the Russian Federation, provides for 2 sections in the asset and 3. N 57n are included in the form. The form of the Balance Sheet was approved by the order of the Ministry of Finance of Russia dated July 2, 2010. Further, in the form of the balance sheet, form 1. Explanations drawn up in the tabular form of Appendix 3 to Order of the Ministry of Finance of Russia 66n. Approve attached

Ministry of Finance. The form of the balance sheet was approved by order of the Ministry of Finance of Russia dated July 2, 2010 The form of the balance sheet netto, approved by the Ministry of Finance of the Russian Federation, provides for 2 sections in the asset and 3. N 57n are included in the form. The form of the Balance Sheet was approved by the order of the Ministry of Finance of Russia dated July 2, 2010. Further, in the form of the balance sheet, form 1. Explanations drawn up in the tabular form of Appendix 3 to Order of the Ministry of Finance of Russia 66n. Approve attached  ... To approve the forms of the balance sheet and the report on financial results in accordance with Appendix No. 1 to this order. To approve the forms of the balance sheet and the statement of financial results 2018 2019 in accordance with Appendix No. 1 to this. Fixed assets 1130 Difference between account balances 01. RUSSIAN POST online SERVICES. It is the basis for understanding a key financial statement known as the balance sheet. It is, as before, approved by order of the Ministry of Finance of Russia dated July 02, 2010 66n. Of the Ministry of Finance of Russia from October 5, 2011 124n Rossiyskaya Gazeta, 291, about the order. Ministry of Finance of Russia from 34n, as amended by The form of the balance sheet form code according to OKUD was approved by the order of the Ministry of Finance of Russia dated July 2, 2010. The accounting methodological center of the BMC is developing them. Balance sheet in accordance with Appendix 2 to this order. Included in the interim and annual financial statements, the balance sheet shall be considered form 1. Order of the Ministry of Finance of Russia from N 57n. The balance sheet form for 2014 was approved by the Order of the Ministry of Finance of Russia dated 66n as amended by This Order is valid from the annual financial statements for 2011. The balance sheet contains two parts of the asset and the liability, which should be. Approve the balance sheet forms and. The paragraph has become invalid by the order of the Ministry of Finance of Russia dated 04. Forms of financial statements that are absent in. The rules for evaluating items have been approved by the Government of Russia, and the main principle here is the assessment of the balance sheet. Form 3 of the balance sheet is a report on. In the form of the balance sheet approved by the order of the Ministry of Finance of the Russian Federation On the forms of financial statements of organizations dated July 2, 2010. On the forms of financial statements of organizations. LLC or a person who took

... To approve the forms of the balance sheet and the report on financial results in accordance with Appendix No. 1 to this order. To approve the forms of the balance sheet and the statement of financial results 2018 2019 in accordance with Appendix No. 1 to this. Fixed assets 1130 Difference between account balances 01. RUSSIAN POST online SERVICES. It is the basis for understanding a key financial statement known as the balance sheet. It is, as before, approved by order of the Ministry of Finance of Russia dated July 02, 2010 66n. Of the Ministry of Finance of Russia from October 5, 2011 124n Rossiyskaya Gazeta, 291, about the order. Ministry of Finance of Russia from 34n, as amended by The form of the balance sheet form code according to OKUD was approved by the order of the Ministry of Finance of Russia dated July 2, 2010. The accounting methodological center of the BMC is developing them. Balance sheet in accordance with Appendix 2 to this order. Included in the interim and annual financial statements, the balance sheet shall be considered form 1. Order of the Ministry of Finance of Russia from N 57n. The balance sheet form for 2014 was approved by the Order of the Ministry of Finance of Russia dated 66n as amended by This Order is valid from the annual financial statements for 2011. The balance sheet contains two parts of the asset and the liability, which should be. Approve the balance sheet forms and. The paragraph has become invalid by the order of the Ministry of Finance of Russia dated 04. Forms of financial statements that are absent in. The rules for evaluating items have been approved by the Government of Russia, and the main principle here is the assessment of the balance sheet. Form 3 of the balance sheet is a report on. In the form of the balance sheet approved by the order of the Ministry of Finance of the Russian Federation On the forms of financial statements of organizations dated July 2, 2010. On the forms of financial statements of organizations. LLC or a person who took  ... Approve the attached Scope Guidelines. Since 2018, as part of fixed assets, leave only property on the balance sheet, which is considered an asset. Order of the Ministry of Finance of Russia from N 66n ed. Appendix The standard form of the balance sheet has been approved. Leaving unsettled on the balance sheet. Ministry of Finance Order of the Ministry of Finance of Russia dated 66n On accounting forms. To approve the forms of the balance sheet and the statement of financial results in accordance with Appendix 1 to the Ministry of Finance of Russia dated July 1, 2013

... Approve the attached Scope Guidelines. Since 2018, as part of fixed assets, leave only property on the balance sheet, which is considered an asset. Order of the Ministry of Finance of Russia from N 66n ed. Appendix The standard form of the balance sheet has been approved. Leaving unsettled on the balance sheet. Ministry of Finance Order of the Ministry of Finance of Russia dated 66n On accounting forms. To approve the forms of the balance sheet and the statement of financial results in accordance with Appendix 1 to the Ministry of Finance of Russia dated July 1, 2013  ... The balance sheet form was approved by the Ministry of Finance of the Russian Federation in order to regulate the accounting one. Order of the Ministry of Finance of Russia 66n. The approved form of the balance sheet c. FORMS OF ACCOUNTING BALANCE SHEET AND REPORT ON PROFITS AND LOSSES as revised. N 34n, determines the order of reflection. Balance sheet and report forms. Changes have been made to the balance sheet form starting from the annual financial statements for 2011. In 2013, a resolution was adopted, approved by the Ministry of Finance of Russia, according to which all business

... The balance sheet form was approved by the Ministry of Finance of the Russian Federation in order to regulate the accounting one. Order of the Ministry of Finance of Russia 66n. The approved form of the balance sheet c. FORMS OF ACCOUNTING BALANCE SHEET AND REPORT ON PROFITS AND LOSSES as revised. N 34n, determines the order of reflection. Balance sheet and report forms. Changes have been made to the balance sheet form starting from the annual financial statements for 2011. In 2013, a resolution was adopted, approved by the Ministry of Finance of Russia, according to which all business  ... It is important that all forms of financial statements are approved by Order of the Ministry of Finance of the Russian Federation 66 of 2010, in the latter. ORDER OF THE MINISTRY OF FINANCE OF RUSSIA FROM 02. The balance sheet is approved by order of the Ministry of Finance of Russia dated 66n. The Ministry of Finance of Russia made changes to the order of 66n On the forms of financial statements of organizations. Accounting, bookkeeping is an orderly system for collecting, registering and summarizing information in monetary terms about the state of property, liabilities and capital of the organization and their changes by continuous, continuous and documentary reflection of all business transactions. Balance sheet form 2017, a sample of which is presented.

... It is important that all forms of financial statements are approved by Order of the Ministry of Finance of the Russian Federation 66 of 2010, in the latter. ORDER OF THE MINISTRY OF FINANCE OF RUSSIA FROM 02. The balance sheet is approved by order of the Ministry of Finance of Russia dated 66n. The Ministry of Finance of Russia made changes to the order of 66n On the forms of financial statements of organizations. Accounting, bookkeeping is an orderly system for collecting, registering and summarizing information in monetary terms about the state of property, liabilities and capital of the organization and their changes by continuous, continuous and documentary reflection of all business transactions. Balance sheet form 2017, a sample of which is presented.

Tags: form, approved by russia, ministry of finance, accounting, balance

Form 0504206 Memorandum for accountable money sample