Fixed assets under the simplified tax system: accounting in the ledger of income and expenses

The procedure for writing off expenses for the acquisition of fixed assets under the simplified taxation system depends on the service life of the property and the moment of its purchase (before or after the transition to a special mode). Let's represent it in the form of a diagram:

* The amounts spent on the purchase of fixed assets can be taken into account only by those organizations on the simplified tax system that have chosen the object "income minus expenses".

As you can see, fixed assets under the simplified tax system can be written off in different ways. Therefore, reflecting transactions on property in the ledger of income and expenses, you can be mistaken. To avoid this, in the article we will show with examples how to fill out the book of income and expenses in this or that case. Note that from January 1, 2013, the accounting book must be kept in the form approved by the order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n.

Fixed assets under simplified taxation system in the ledger of income and expenses

To begin with, let's decide what belongs to fixed assets according to the rules of chapter 26.2 of the Tax Code of the Russian Federation. Let's turn to paragraph 4 of article 346.16 of the code. It says that in this case it is necessary to use the provisions of Chapter 25 of the Tax Code of the Russian Federation. Among other things, this means that the initial value of the property should be more than 40,000 rubles. Only in this case it is taken into account as a fixed asset.

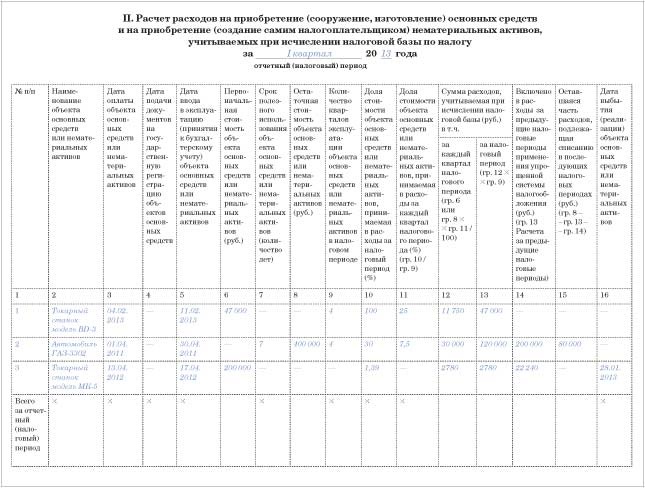

Now about in which section of the book you will show the costs associated with the purchase of fixed assets. Section II is reserved for this. Calculate here for each object separately. After all, the terms of service may differ, which means that the write-off procedure will be different.

The general rules for filling out Section II are as follows. Reflect the information for each reporting (tax) period. That is, first you will enter data for the first quarter, then for half a year, 9 months and a year. Make entries for the last date of the reporting or tax period.

Then you will transfer the totals from the last line in the table of section II to section I of the book, namely to column 5 "Expenses taken into account when calculating the tax base". The record will need to be transferred to the last day of the quarter.

Accounting for fixed assets purchased under the simplified tax system

You can write off the cost of fixed assets purchased in the special mode in full during the year in equal installments. Naturally, after reflecting such property on account 01 "Fixed assets". Well, on the prerequisite that you paid off with the supplier.

We emphasize: it is better to reflect the costs of the purchase of a fixed asset evenly. This is the approach that representatives of the Ministry of Finance of Russia recommend using in a letter dated March 27, 2012 No. 03-11-11 / 103.

Show the part of the expenses that you write off in each quarter in column 11 of section II of the book. But the service life of the fixed asset in this case does not matter. Therefore, you do not have to fill in column 7 of section II of the book.

When you determine how much expenses to write off in a particular period, take into account the value of the property with VAT. After all, your company does not pay this tax and does not reimburse it from the budget. And according to the rules of PBU 6/01 - it is according to them that the initial cost of the property purchased on the simplified system is formed - non-refundable taxes must be included in such a cost. Fixed assets under the simplified taxation system are accounted for together with input VAT. This tax is not a separate expense.

Example

LLC "Vega" applies a simplified taxation system since January 1, 2013 and determines the tax on the difference between income and expenses. Before the simplification, the company applied the general taxation regime. In February 2014, the company purchased a lathe (model BD-3) for RUB 47,000. (in view of VAT). In the same month, Vega LLC put the machine into operation and transferred the payment to the supplier. That is, all the conditions for recognizing an expense have been met.

Since the company acquired fixed assets under the simplified tax system, the cost of this property can be completely written off in 2014.

Every quarter, starting from March 31, the accountant will evenly charge the cost of the purchased machine. Section II of the book of accounting for income and expenses in the simplified form, he filled in as follows:

Accounting for fixed assets purchased before the simplified tax system

Let's deal with those fixed assets that the company bought before switching to simplification. How quickly you write off its cost depends on how long such an object can serve: no more than 3 years, from 3 to 15 or more than 15 years. You determine the term according to the Classification approved by the Decree of the Government of the Russian Federation of January 1, 2002 No. 1. In any case, the residual (!) Value of the fixed asset must be taken into account. That is, the one that was registered in tax accounting on the day from which you began to apply the simplified tax system. Typically, this is January 1st. It is this amount that must be indicated in column 8 of section II of the book.

Service life does not exceed 3 years

Fixed assets with a term of use no more than 3 years can be written off to expenses in the first year of the application of the simplified taxation system. But again, evenly.

That is, the write-off procedure in this case is similar to the one that should be applied to the property purchased during the simplification process. But there you take into account the initial cost of the object. And here, we repeat, - the residual.

Service life is from 3 to 15 years inclusive

You have established that the purchased property belongs to a group of objects with a period of use from 3 to 15 years. In this case, you will write off the residual value of the fixed asset as an expense within 3 years. Moreover, in the first year of using the simplified code, half the cost can be taken into account. In the second year - 30 percent. You will write off the remaining 20 percent within the third year.

At the same time, within each year, recognize expenses evenly - at the end of the quarter. Show the share of expenses that relates to the current year in column 10 of section II of the book.

Example

Let's use the conditions of the previous example. As of January 1, 2013, that is, on the date of transition to the simplified tax system, fixed assets are registered in the tax accounting records of Vega LLC. This is a car (model GAZ-3302) with a residual value of 400,000 rubles.

The service life of the machine is 7 years. This is provided for by the Classification. Therefore, under simplification, the property must be written off within three years.

In 2013, OOO Vega wrote off half of the residual value of the car as an expense. And in 2013 it will be able to take into account 30 percent of the cost, that is, 120,000 rubles. (30,000 rubles each quarter). The accountant reflected these expenses in section II of the book /

Service life exceeds 15 years

The residual value of those fixed assets that will last more than 15 years, and will have to be written off within 10 years, and evenly.

Accounting for transactions on the sale of fixed assets under the simplified tax system

Your company can not only buy property, but also sell old property. Such transactions, of course, must also be recorded in the ledger of income and expenses (section II). But exactly what amounts you reflect depends on how long the property has worked for your organization.

If the fixed asset has served the company for less than 3 years (and when it is an object of the seventh-tenth depreciation groups - less than 10 years), then the amounts previously accounted for in expenses will have to be recalculated. Are you selling property that has been in use for longer? Then no adjustments are needed. Let's consider both options in more detail.

The property has served for at least three (10) years

Suppose that on the day the asset is sold, its actual service life has exceeded 3 years. Or 10 years - if we are talking about objects of the seventh-tenth depreciation groups.

As we said before, you do not have to adjust costs in this case. Just on the day when the payment is received from the buyer, reflect the entire amount received in column 4 of section I.

The principal has been used for less than three (10) years

If the property has served you for less than 3 years (10 years - for fixed assets of the seventh to tenth depreciation groups), you will have to recalculate the tax base for the simplified taxation system.

Moreover, the recalculation must be done, even if you managed to write off the cost of the fixed asset in full. The originally set service life is irrelevant.

How do you do the conversion? First, determine the amount of depreciation deductions according to the rules of Chapter 25 of the Tax Code of the Russian Federation. Moreover, it was precisely for those years when you attributed the cost of a fixed asset to expenses, using a simplification. Then the resulting depreciation amount must be compared with the expenses written off under the simplification. If depreciation according to the rules of income tax turns out to be less than the amounts that you took into account in due time, then you will have to pay arrears, penalties and submit revised declarations for previous years.

There are no special sections in the book where you could reflect the recalculation of the base. Therefore, in such cases, draw up certificates in free form. This help might look like this:

In the book, in section II, it is necessary for reference to indicate on what date you sold the fixed asset (column 16). In addition, reflect and the amount of depreciation charges accrued according to the rules of chapter 25 of the code and relating to this year. Indeed, when calculating income tax, depreciation is charged for the month in which the property was sold.

Example

Let's use the conditions of the first example. In April 2013, the company acquired a lathe (model MK-5) for RUB 200,000. (in view of VAT). The service life of the machine is 6 years (72 months). In the same month, OOO Vega put the machine into operation and paid for it to the supplier. Since the company acquired the fixed asset during the simplification process, its cost was written off completely to expenses in 2013 (evenly during the II, III and IV quarters, that is, 66,666.67 rubles each).

In January 2014 Vega LLC sold the machine. Since the actual service life was less than three years (9 months - from May 2013 to January 2014), the accountant recalculated the tax base for 2013 simplified. At the same time, the accountant accrued depreciation on a straight-line basis for January 2014. The amount of depreciation deductions is 2,780 rubles. (200,000 rubles × 1.39%) per month. In 2013, depreciation amounted to 22,240 rubles. (2780 rubles × 8 months). The accountant showed this amount in section II.