Doubtful receivables balance sheet formula. Accounts receivable turnover calculation. Accounts receivable turnover. economic sense

Accounts receivable - debt of organizations and individuals this organization (for example, debts of buyers for purchased goods or services rendered, debts of accountable persons for the amounts of money issued to them) Accordingly, the organization and persons who are debtors of this organization are called debtors.

Accounts receivable management involves, first of all, planning and control over the turnover of funds in the calculations. The acceleration of turnover in dynamics is regarded as a positive trend. Of great importance are the selection of potential buyers and the determination of the terms of payment for the goods provided for in the contracts.

A generalizing indicator of debt repayment in financial analysis is turnover. The liquidity indicator characterizes the speed with which it will be turned into cash(availability). Thus, the indicator of quality and liquidity accounts receivable it could be turnover.

The turnover ratio is calculated as the ratio of the volume of income (revenue) from the sale of products (works, services) to the average receivables according to the formula:

The code. = DR / DZ, where

The code. - the turnover ratio of receivables;

DR - income from the sale of products (works, services);

DZ - average receivables.

This coefficient shows how many times the debt is formed and received by the enterprise during the period under study.

Accounts receivable turnover (AR) can also be calculated in days. This indicator reflects the average number of days required for its return. It is calculated as the ratio of the number of days in the period and the turnover ratio:

OD \u003d P / Cob, where

P is the duration of the period;

An increase in the receivables turnover ratio indicates a relative decrease in commercial lending and vice versa. It is desirable to maximize this indicator. An increase in the indicator indicates an improvement in the management of receivables.

Accelerating the turnover of receivables is a priority for enterprises in modern conditions and is achieved in various ways.

At the stage of creation production stocks these may be:

Implementation of economically justified reserve norms;

Bringing suppliers of raw materials, service components, etc. closer to consumers;

Widespread use of direct long-term connections;

Expansion of warehouse logistics systems, as well as wholesale trade materials and equipment;

Integrated mechanization and automation of loading and unloading operations in warehouses.

At the stage of work in progress;

Acceleration scientific and technological progress(introduction of advanced equipment and technology, especially waste-free and low-waste, robotic systems, etc.)

Development of standardization, unification, optimization;

Improving the forms of organization of industrial production, the use of cheaper structural materials;

Improving the system of economic incentives

economical use of raw materials and fuel and energy resources;

Increase in the share of products in high demand.

At the stage of treatment;

Approximation of consumers of products to its manufacturers;

Improving the settlement system;

Increase in volumes products sold due to the fulfillment of orders through direct communications, early release of products, production of products from saved materials;

Careful and timely selection of shipped products by batches, assortment, transit rate, shipment in strict accordance with the concluded contracts.

Accounts receivable - an element of working capital, its reduction reduces the coverage ratio. Therefore, it is necessary to solve not only the problem of reducing accounts receivable, but also balancing it with accounts payable. When analyzing the relationship between receivables and payables, it is necessary to analyze the conditions commercial loan provided to the company by suppliers of raw materials and materials.

You can analyze the effectiveness of the above methods using the financial analysis program FinEk Analysis.

Example. Analysis of the business activity of the Enterprise as of 01.01.2007

| 1. The coefficient of the total turnover of property (resources) (D1) characterizes the rate of turnover (in the number of turnovers per period) of the entire property of the enterprise. | |||

| Page 010 (Form No. 2) | D1previous | 2.321 | |

| (p.300j+p.300n)/2 | D1 reporting | 2.516 | |

| The change | 0.195 | positive trend | |

| The overall turnover of property (resources) in reporting period compared to the previous period. | |||

| 2. The turnover ratio of mobile assets (D2) characterizes the rate of turnover of all current assets of the enterprise (both material and monetary). | |||

| Page 010 (Form No. 2) | D2previous | 4.181 | |

| (p.290n+p.290j)/2 | D2 reporting | 4.069 | |

| The change | -0.112 | negative trend | |

| The turnover of all working capital is reduced. | |||

| 3. Inventory turnover ratio (D3), based on sales, shows the number of inventory turnover for the analyzed period. | |||

| Page 010 (Form No. 2) | D3previous | 5.267 | |

| (p.210j+p.210n)/2 | D3reporting | 5.326 | |

| The change | 0.059 | positive trend | |

| Inventory turnover increases based on sales volume. | |||

| 3.1. The inventory turnover ratio (D3.1), based on the volume of costs, including the cost of goods sold, products, works, services, as well as commercial and administrative expenses, shows the number of inventory turnovers for the analyzed period. | |||

| Line 020+line 030+line 040 (Form No. 2) | D3.1previous | 4.675 | |

| (p.210j+p.210n)/2 | D3.1 reporting | 4.78 | |

| The change | 0.105 | positive trend | |

| Inventory turnover is reduced, based on the volume of costs. | |||

| 4. Cash turnover ratio (D4) characterizes the rate of cash turnover. | |||

| Page 010 (Form No. 2) | D4previous | 214.428 | |

| (p.260n+p.260j)/2 | D4reporting | 183.041 | |

| The change | -31.387 | negative trend | |

| The turnover of all cash is reduced. | |||

| 5. The turnover ratio of funds in the calculations (total receivables) (D5) characterizes the expansion or reduction of commercial credit provided by the enterprise. The value of this coefficient at enterprises is especially high at the present time, in conditions of non-payments. | |||

| Page 010 (Form No. 2) | D5 previous | 26.251 | |

| ((p.230k+p.240k)+(p.230n+p.240n))/2 | D5 reporting | 20.078 | |

| The change | -6.173 | negative trend | |

| The turnover of funds in settlements is reduced. The diversion of enterprise funds, in the form of receivables, from economic turnover is increasing. The lending of these funds to other enterprises is increasing. The losses of the enterprise from inflationary provision of receivables are increasing. | |||

| 5.1. The turnover ratio in settlements (accounts receivable, payments on which are expected more than 12 months after reporting date) (D5.1). characterizes the expansion or decline of commercial credit provided by the enterprise. | |||

| Page 010 (Form No. 2) | D5.1previous | 0 | |

| (p.230n+p.230j)/2 | D5.1 reporting | 0 | |

| The change | 0 | ||

| During the entire analyzed period, there were no accounts receivable, payments for which are expected more than 12 months after the reporting date. | |||

| 5.2. The turnover ratio of funds in settlements (accounts receivable, payments on which are expected within 12 months after the reporting date) (D5.2), characterizes the expansion or reduction of a commercial loan provided by the enterprise. | |||

| Page 010 (Form No. 2) | D5.2previous | 26.251 | |

| (p.240n+p.240j)/2 | D5.2 reporting | 20.078 | |

| The change | -6.173 | negative trend | |

| The turnover of funds - receivables, payments on which are expected within 12 months after the reporting date, is decreasing. The diversion of funds of the enterprise is increasing, in the form of this type of receivables from economic turnover. The lending of these funds to other enterprises is increasing. | |||

| 6. The turnover period of funds in the calculations (D6) characterizes the average maturity of all receivables in days: | |||

| D6 = Analysis period(days)/D5 | D6previous | 13.7 | days |

| period | D6reporting | 17.9 | days |

| The change | 4.2 | negative trend | |

| Increasing the period of turnover of funds in the calculations - all receivables. Negative trend. | |||

| 6.1. The turnover period of receivables, payments for which are expected more than 12 months after the reporting date, characterizes the average maturity of these receivables in days: | |||

| D6.1 = Analysis period(days)/D5.1 | D6.1previous | 0 | |

| period | D6.1 reporting | 0 | |

| The change | 0 | ||

| During the entire analyzed period, there were no accounts receivable, payments on which are expected more than 12 months after the reporting date. | |||

| 6.2. The turnover period of receivables, payments for which are expected within 12 months after the reporting date, characterizes the average maturity of these receivables in days: | |||

| D6.2 = Analysis period(days)/D5.2 | D6.2previous | 13.7 | days |

| period | D6.2 reporting | 17.9 | days |

| The change | 4.2 | negative trend | |

| The turnover period of receivables is increased, payments on which are expected within 12 months after the reporting date. Negative trend. | |||

| 7. Turnover ratio accounts payable characterizes the expansion or decline of commercial credit provided to the enterprise. | |||

| Page 010 (Form No. 2) | D7previous | 8.604 | |

| (p.620n+p.620j)/2 | D7 reporting | 7.822 | |

| The change | -0.782 | negative trend | |

| The turnover of accounts payable is reduced. The enterprise began to use the funds of other enterprises in its turnover to a greater extent. | |||

| 8. The turnover period of accounts payable characterizes the average period of repayment of the company's debts for current liabilities in days: | |||

| D8 = Analysis period(days)/D7 | D8previous | 41.8 | days |

| period | D8reporting | 46 | days |

| The change | 4.2 | negative trend | |

| Increases the turnover period of accounts payable. The company has slowed down the settlement of its current liabilities. Negative trend. | |||

| 9. Turnover ratio equity characterizes the rate of turnover of own capital. | |||

| Page 010 (Form No. 2) | D9previous | 4.95 | |

| (p.490n+p.490j)/2 | D9reporting | 5.082 | |

| The change | 0.132 | positive trend | |

| Increasing equity turnover. | |||

| 10. Recoil ratio intangible assets characterizes the effectiveness of the use of intangible assets. | |||

| Page 010 (Form No. 2) | D10previous | 10711.344 | |

| (p.110n+p.110j)/2 | D10reporting | 14075.833 | |

| The change | 3364.489 | positive trend | |

| Efficiency of use of intangible assets increases. | |||

| 11. Capital productivity of fixed assets characterizes the efficiency of the use of fixed assets of the enterprise. | |||

| Page 010 (Form No. 2) | D11previous | 5.328 | |

| (p.120n+p.120j)/2 | D11 reporting | 6.778 | |

| The change | 1.45 | positive trend | |

| Efficiency of use of fixed assets increases. | |||

| 12. Duration financial cycle(D12) shows during what period the company's funds should be reimbursed in the form of the cost of goods produced or services rendered, and stocks and accounts payable should be sold in the form of the cost of goods manufactured or services rendered. The longer the financial cycle, the higher the need for working capital | |||

| D12 = D6+T/D3.1-D8 | D12previous | 48.9 | days |

| D12 reporting | 47.2 | days | |

| The change | 1.7 | negative trend | |

| Increasing the duration of the financial cycle, decreasing investment attractiveness enterprises. | |||

Accounts receivable is an integral element of the marketing activities of any enterprise. Too high share of receivables in overall structure assets reduces the liquidity and financial stability of the enterprise and increases the risk of financial losses of the company. The prudent use of commercial credit contributes to sales growth, an increase in market share and, as a result, a positive effect on financial results companies.

Within the framework of this article, the receivables turnover ratio is considered - the calculation formula, the meaning of the concept and its main parameters. We will also explain in an accessible language how receivables differ from accounts payable and why it is important for enterprises to track the dynamics of these indicators.

The meaning of the term "accounts receivable"

Accounts receivable are all debts of enterprises and individuals in relation to the organization. That is, when the organization has already shipped goods or provided services, but has not yet received payment for them, receivables arise. To put it even more simply, this is the money that the company owes. Among specialists, the term is usually shortened to the common parlance "accounts receivable".

Such unpaid obligations indirectly indicate the losses of the enterprise.- after all, the goods have already been delivered, services have been provided, resources have been spent on them, but compensation has not been received. Money cannot be directed into circulation, which slows down the development of the company. Moreover, there is a risk of not receiving payment at all, for example, in the event of the bankruptcy of the acquiring company.

The company's debtors are called "debtors". In this capacity, they can act as entire organizations, legal entities, individual entrepreneurs as well as individual individuals. Virtually every enterprise has such a debt and in itself does not indicate anything.

Virtually every enterprise has such a debt and in itself does not indicate anything.

Varieties of receivables

There are several main options for the appearance of "receivables":

- The most common option is delayed payment for goods delivered and services rendered from contractors.

- Errors in settlements with employees, for example, erroneously overstated payments wages, per diem or travel allowance. The funds that the employee will have to return are recorded in the value of receivables.

- Prepayment for goods and services of other organizations.

- Non-payment of founders when contributing to the authorized capital.

Does it make sense to insure "receivables"

Unpaid debt threatens the organization with losses, therefore many financial executives are thinking about insuring "receivables". This option is beneficial to the organization, but not mandatory from the point of view of the law.

If, nevertheless, a decision is made about insurance, find insurance company won't be a big problem. There are many companies on the market offering similar services. For insurance, you need to fill out the following documents:

- a complete list of the company's counterparties who may be indebted;

- questionnaire about legal entity covering, among other things, the issues of his financial condition.

The meaning of the term "accounts payable"

People who are not related to accounting sometimes confuse the concept of receivables and payables. When should the enterprise itself, and when should it? The term "accounts payable" refers to all the debts of the enterprise. That is, the accounts receivable shows how much the company owes, and the accounts payable shows how much the company itself owes.

Who can an organization owe? Generally, there are 3 main options:

- Debts to other organizations - for raw materials, goods and services - or to banks.

- Delays in the payment of wages, as well as dividends to shareholders and founders.

- On obligatory payments and taxes to the budgets of all levels.

The presence of accounts payable in the organization is a completely normal working condition, which does not speak about the problems and tendencies towards bankruptcy. It is important to monitor only the dynamics of changes in this indicator and its relationship with the "accounts receivable" (see the "Comparison of accounts receivable and accounts payable" section).

It is also important to know that debt evasion is punishable by law: from a fine of 200 thousand rubles to imprisonment for up to 2 years. Responsibility is provided for non-payment of amounts from one and a half million rubles.

It is important to monitor only the dynamics of changes in accounts payable and its relationship with "receivables".

The economic meaning of receivables

By the presence and value of receivables, one can judge the efficiency of trade between the enterprise and its customers. To do this, it is necessary to calculate the turnover ratio of "receivables" - a value that shows how quickly the company's goods and services turn into money.

The current debt ratio shows new ways for the development of the enterprise, improving the efficiency of commodity-money relations and even reveals risks when trading with certain organizations. First of all, this value should be of interest to the financial director, the head of the sales department, as well as the entire management of the company as a whole.

How to Calculate the Accounts Receivable Turnover Ratio

Now consider how to calculate the value of the turnover ratio of receivables. It's easy to do. The following calculations need to be made:

- sales revenue: average amount of accounts receivable.

Please note that it is the arithmetic mean value of the debt that is needed. That is, for example, if you calculate the coefficient for a quarter, you first need to take debt obligations at the beginning of the quarter, add it to the value at the end of the period and divide by 2.

Formula by data balance sheet will look like this:

- 010 line: 0.5 (230 line at the beginning of the year + 230 line at the end of the year + 240 line at the beginning of the year + 240 line at the end of the year).

Example of calculating the turnover ratio

For clarity, let's analyze a simplified version of the calculation of the turnover ratio of "receivables" for the quarter.

- Calculation of the average value of receivables.

Let's say at the beginning of the quarter the debt is 100,000 rubles, at the end - 50,000 rubles. We consider: (100,000 + 50,000): 2 = 75,000 rubles. - Coefficient calculation. Knowing the average debt and sales revenue, it is easy to calculate the ratio. Let's say the revenue is 1.5 million rubles. We consider: 1,500,000: 75,000 = 20.

The current debt ratio shows new ways for the development of the enterprise

Interpretation of the value of the turnover ratio

The most important thing is not to calculate the coefficient, but to correctly interpret its economic value. The first thing you need to pay attention to is the fact that the normative value of this indicator in different business sectors will differ.

For Agriculture the normal value is 4.8, for the food and processing industries - 8, for trade and others - 12. It is important to monitor the dynamics of the coefficient. An increase in receivables turnover is a good trend.

It is appropriate to compare the turnover with the average values in the market in order to understand how the company's development vector coincides with the general market, as well as with the data of other companies in the industry (however, it is virtually impossible to find out this information, it is actually part of a trade secret).

Calculation of the turnover ratio of accounts payable

This indicator will show how many trade turnovers are needed to pay all invoices issued or how many times the company has paid off creditors during the reporting period. It is easy to calculate it. Divide the cost of all goods sold by average value creditor payments, that is:

- cost of goods sold (services rendered): average amount of accounts payable.

There is no unambiguous interpretation of this indicator; it is important to evaluate it in dynamics. A good indication is the increase in the indicator - this means that the turnover of sales and the provision of services are growing. In any case, it is important to compare the parameter with a similar receivables ratio.

There is no unambiguous interpretation of the accounts payable turnover ratio; it is important to evaluate it in dynamics.

Comparison of receivables and payables

one more important indicator, characterizing the financial side of the company's activities, is the ratio of accounts receivable and accounts payable. Calculating this indicator is quite simple: the total amount of receivables must be divided by the total amount of accounts payable.

For example, the amount of accounts receivable is 1,000,000 rubles, the amount of accounts payable is 500,000 rubles. In this case, 1,000,000: 500,000 = 2. That is, the ratio is "2". How to interpret this value?

The optimal value is considered to be a number from 0.9 to 1, that is, a situation where two types of debts are approximately equal to each other. Most companies operate in this mode.

However, some economists believe that companies should strive to exceed the "receivables" by about 2 times, that is, the value of the coefficient in the range of 1.9 and 2.1.

What is a "short-term debt ratio"

To monitor the financial condition of a company, it is also important to know the concept of "coefficient short-term debt". As the name implies, this indicator characterizes the company's short-term liabilities. It is used to assess the risk of bankruptcy of the organization. Now let's calculate the short-term debt ratio. The formula for balance might look like this:

- Total debt: total assets.

- (590 line + 690 line) : 699 line.

Conclusion

The calculation of the turnover ratio of receivables and payables is necessary to monitor the financial condition of the organization, prevent risks and even predetermine the threat of bankruptcy. The normative value of these indicators is different for different business sectors.

The formula for calculating the turnover of receivables from textbooks on financial analysis has drawbacks, besides, in practice, financiers make mistakes in its application. We propose an adjusted calculation method.

The formula for calculating the turnover of receivables

For calculation, the standard formula for the receivables turnover ratio, described in most textbooks on financial analysis, is usually used:

ODZ \u003d ((DZn: 2 + DZk: 2) : B) KD

- ODZ - receivables turnover period in days;

- DZn and DZk - its size, respectively, at the beginning and end of the period in rubles;

- B - revenue in rubles;

- CD - the number of days in the period.

This formula has drawbacks, besides, in practice, financiers make mistakes when applying it. The most common is the use of the indicator " net proceeds» from the income statement, i.e. revenue less indirect taxes (VAT and excises). Since the receivable contains indirect taxes, the problem of incompatibility of indicators arises. Then the calculated period of its turnover looks worse than it actually is, especially if the company is an excise payer, which hinders effective receivables management .

But even when the correct value is substituted as revenue, this indicator can be significantly distorted. The fact is that the proceeds from the sale of products, as a rule, is determined "by shipment", and decrease in turnover occurs at the time of receipt of funds. Shipment of products entails an increase in receivables and at the same time improves turnover. At the same time, there may not be a real reduction in the turnover period, since the payment for the shipped goods is not received. The problem is typical for companies that aggressively increase sales by increasing payment deferrals for customers. Consider next an example of a calculation.

Example of calculating the turnover period

Within three months (January-March), the company increases sales, while the receipt of money for shipped products decreases every month (see table) and receivables grow like an avalanche.

Line 4 calculates the turnover period using the above formula. Despite the decrease in the volume of payments for shipped products with a simultaneous increase in shipments, the situation appears to be positive. So, in March, the value was 23 days, that is, theoretically, the receivables formed in March will be repaid within the specified time frame. In reality, at the end of March, it significantly exceeds the amount of funds received, and if the trend continues, it will take more than two months to repay (provided that shipments are even throughout March). That is, the turnover indicator, calculated on the basis of revenue "by shipment", in this case does not provide objective information.

Even when buyers stop paying for products altogether, this figure may look acceptable until the company stops shipping. This is the key drawback of the traditional approach.

Table.Comparison of turnover rates

| p/p | Indicator | 2016 | 2017 | ||

| At the end of the year | January | February | March | ||

| 1 | Accounts receivable at the end of the period, thousand rubles | 1100 | 900 | 1050 | 2650 |

| 2 | (“on shipment”), thousand rubles | 900 | 1100 | 2500 | |

| 3 | Receipt of funds for shipped products, thousand rubles | 1100 | 950 | 900 | |

| 4 | Turnover period, in days (using revenue "by shipment") | 34 | 25 | 23 | |

| 5 | Accounts receivable turnover period, days (receipt of funds for shipped products) | 28 | 29 | 64 | |

The turnover period should show how long the shipped goods will be fully paid for. However, the calculation in the manner described above, rather, reflects the relationship between receivables and the cost of shipped products. And the turnover indicator becomes quite accurate only with the uniformity of shipments and payments for a long time.

Inaccuracies can be avoided if instead of the revenue "on shipment" we substitute the amount of cash received for the delivered products into the formula for calculating the turnover ratio of receivables. The CFO can then more accurately forecast cash flow and debt for the coming periods, even seasonally adjusted (see also cash flow forecasting model in excel ). This means that the company will be able to correctly assess its need for loans or the possibility of their repayment, calculate the cost of debt financing and improve the quality of planning.

The results of calculations using the indicator "Receipt of funds for shipped products" are shown in line 5 of the table. If we compare them with the data of line 4, then the differences are obvious. In most cases, the accounts receivable turnover calculated "on receipt of funds" gives much more accurate results. At the same time, it should be noted that the use of this technique will be especially useful for companies whose demand for goods is subject to significant seasonal fluctuations, as well as organizations that aggressively increase sales volumes. In addition, it allows you to more accurately analyze the effectiveness of debt management in the context of individual customers, channels or markets.

The formula for calculating the turnover of accounts receivable in days

A more common and understandable option in practice is the debt repayment period in days.

ODZ in days = (DZs x 365) / V

where ODZ is the turnover of receivables in days;

DZs - average debt;

B is revenue.

This ratio will show how long the accounts receivable last in days on average. The lower the ratio, the better for the supplier company. It is advisable to compare the indicator with the average period of deferred payment for buyers. Let's say the resulting value is 60 days, and in accordance with the company's business practice, a deferred payment is granted to customers for 30 days. Consequently, counterparties systematically violate the terms of payment. As a result, the funds of the organization are diverted from circulation. This company is in dire need of a fix. credit policy and business process optimization interactions with buyers.

Average receivables repayment period

The CFO should also review the average receivables repayment period at least once a week. This will ensure that lending and debt collection are carried out properly. The speed at which a company can receive customer payments on outstanding balances is critical to reducing the need for cash.

A very short receivables collection period indicates that the company's lending and collection functions are working very well in terms of avoiding potentially problematic customers and receiving late payments. This indicator is especially useful when compared with the standard term of credit given to buyers. For example, if the average repayment period is 60 days and the loan term is 30 days, buyers are taking too long to pay their bills. A sign of good performance is when the average repayment period is only a few days longer than the standard loan term.

Accounts receivable period formula

Accounts Receivable Period = Average Accounts Receivable / (Annual Sales / 365)

Consider an example. The CFO of Flexo Paneling Company, a manufacturer of modular office equipment, wants to determine the repayment period for receivables. In the reporting period in June, the incoming receivables balance was $318,000 and the outgoing balance was $383,000. Sales for May and June totaled $625,000.

Based on this data, the CFO calculates the average maturity as follows:

Notice that the CFO got annual sales in the denominator by multiplying the two-month sales period in May-June by six. Given that the company has a set payment period of 30 days after invoicing, a receivables collection period of 34.1 days seems reasonable.

How to manage accounts receivable turnover

Initially, it is important to think in advance which customers the company provides a deferred payment (how to understand whether to believe the buyer who asks for a deferred payment ). It is logical to do this for long-standing and reliable customers. This will avoid the occurrence of overdue receivables.

Deferral of payment must be legally formalized. The contract must specify the persons authorized to draw up such an agreement, the responsibility of the parties, the timing of the calculation of supplies, fines, penalties. This document will form the basis for the work on receivables management.

An important task in managing turnover is the analysis of receivables. Breakdown can be done:

- by clients (key, image, new, potential);

- by regions (at the place of presence of the office, work through representatives, potentially of interest to the regions);

- by managers (managers leading key clients; attracting new partners; promoting new products, etc.);

- on admissible debts (terms are set depending on market conditions and the capabilities of the enterprise).

As part of the work with the turnover of receivables and the analysis of the turnover ratio, the company can offer its punctual partners additional bonuses and discounts. If the counterparty paid on time, the next time he can order a larger volume of goods, get a discount on certain assortment groups, and other bonuses. Such an example will show other counterparties that paying on time is profitable. This approach has a positive effect on financial discipline and partnerships.

VIDEO: How to organize operational control of receivables

Dmitry Ginkulov, Deputy General Director for Economics and Finance of the Artplast company, tells in a video how to organize the operational control of receivables.

Let's figure it out. In the English version, it is called (in the standards of the international financial reporting) – Receivable turnover. This ratio refers to the group of indicators "Business activity" (Turnover). The turnover ratio reflects the intensity (rate of turnover) of the use of assets or liabilities. They determine how the enterprise actively and effectively conducts its activities. Hence the name of the group - "Business Activity".

Accounts receivable

Accounts receivable – monetary obligations enterprises and individuals to our enterprise. For example, we provided a service, shipped goods, but the money has not yet been received by us at the cash desk. Accounts receivable is accompanied by indirect losses in the income of the enterprise. This is explained by the fact that our company has not yet received cash from the rendered services and shipped goods and cannot be put into circulation.

In addition to receivables that can be collected, there is also debt that cannot be collected. It occurs due to:

- liquidation of the debtor,

- bankruptcy of the debtor.

That is why when an enterprise gives money (credits) to other enterprises, it has a credit risk (the risk of not returning receivables). To reduce it, it is necessary to assess the financial stability and liquidity of our counterparty.

Accounts receivable turnover. economic sense

Accounts receivable turnover (equivalent to English: RT, RTR, Receivable turnover, Receivables turnover ratio) is a coefficient characterizing the effectiveness of interaction between the enterprise and contractors. The ratio shows the rate at which a company's goods or services are converted into cash (assets).

Accounts receivable management

The receivables turnover ratio gives an idea of the change in receivables in a positive or negative direction. The main function of receivables management is to increase the receivables turnover ratio. This can be achieved in two ways:

- Increase sales revenue

- Reduce accounts receivable for the period.

To do this, at an early stage of issuing a loan to other enterprises, it is possible to check and evaluate them for financial stability. Three types of credit policy of the enterprise should be distinguished: conservative, moderate, aggressive. With a conservative policy, the company seeks to control its loans as tightly as possible in order to minimize credit risk. With a moderate policy, the company takes on medium credit risk. And with an aggressive policy, the company takes on large credit risks.

Where is the accounts receivable turnover ratio used?

This coefficient is used to determine ways to increase the profitability (profitability) of the enterprise. The main users of the indicator are the general director, commercial director, head of the sales department and sales managers, financial director and financial manager, security service, legal service.

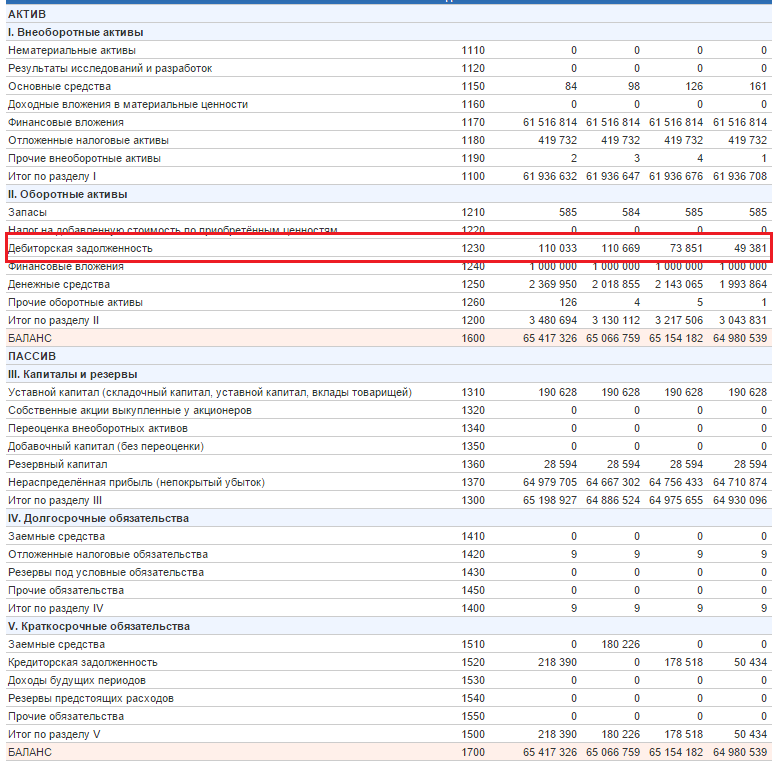

Accounts receivable turnover ratio. Balance Formula

The formula for calculating the receivables turnover ratio is as follows:

Accounts Receivable Turnover Ratio = Sales Revenue/Average Accounts Receivable

Do not forget that the denominator is the average amount, which means that we must take the accounts receivable at the beginning of the period, add it to its value at the end and divide by 2. The formula for calculating the coefficient according to RAS is as follows:

Accounts receivable turnover ratio = line 2110 / (line 1230np. + line 1230kp.) * 0.5

Np. – value of line 1230 at the beginning of the period.

Kp. - the value of line 1230 at the end of the period.

The reporting period may not be a year, but, for example, a month, a quarter. According to the old form of the balance sheet (until 2011), the formula for calculating the coefficient is:

Accounts receivable turnover ratio = line 10 / (line 230 + line 240) * 0.5

Accounts receivable turnover period

Along with the receivables turnover ratio, the receivables turnover period indicator is used. It reflects the number of days required for the conversion of receivables into money supply. The formula for calculating the period of turnover of receivables is as follows:

Accounts receivable turnover period = 360 / Accounts receivable turnover ratio

Instead of 360, you can use 365. The economic meaning of this indicator is to determine the average number of days during which money from the counterparties of the enterprise arrives in its current account.

Video lesson: "Calculation of key turnover ratios for OAO Gazprom"

Calculation of the turnover ratio of receivables on the example of OJSC "Polyus Gold"

Calculation of the accounts receivable ratio for OJSC Polyus Gold. Balance

Calculation of the accounts receivable ratio for OJSC Polyus Gold. Gains and losses report

The normative value of the turnover of receivables

certain normative value coefficient does not. The higher the receivables turnover ratio, the higher the speed of money turnover between our company and the recipients of our goods and services (our counterparties). With a decrease in the value of this coefficient, we can conclude that our partners begin to delay payment for our goods / services. For a better analysis of the receivables turnover, it is useful to calculate its value for the industry on average, as well as for the leader enterprise by this coefficient. So there will be reference values for this coefficient.

Summary

Accounts receivable turnover, important financial indicator, which determines the effectiveness of our company's work with contractors (partners). This coefficient is used for analysis CEO, financial and commercial director, head of sales department, as well as sales and financial managers. An increase in the value of the coefficient indicates that we have increased sales or decreased accounts receivable. The coefficient is directly related to the financial stability of the enterprise and its liquidity: the higher the value, the financial stability and liquidity is better. This is explained by the fact that we quickly receive money for our goods / services and quickly include them both in production turnover and to pay off our debts.