Single simplified tax return sample filling

A simplified declaration in the absence of activity 2015 is filed and filled in by taxpayers in the absence of activity for a certain tax period, one of the convenience of filing is that it is possible to combine several taxes in one document, besides, it is very simple to fill out and the form contains only 2 sheets. Consider who submits such reports, for what taxes, and also consider the situation if the reports were sent by mistake. At the end of the article, you can download the declaration form in the form of KND 1151085.

A single simplified tax declaration can be submitted by persons who are recognized as taxpayers for one or several types of taxes, subject to the following conditions:

- In the absence of transactions and the movement of funds on them on the current accounts and at the taxpayer's cash desk.

- There is no sale of goods (works of services), as a result of which there is an object of taxation for these taxes.

If these conditions are met, we can say that, in fact, no activity is being carried out.

You can submit a single tax return for the following taxes:

- Income tax paid by organizations.

- Personal income tax (only for individual entrepreneurs).

According to the letter of the Ministry of Finance of the Russian Federation, No.АС-4-3 / 12847 dated 08.08.2011, it is possible to submit a single declaration using the simplified tax system.

Deadlines for filing a single declaration and where it is submitted

A unified simplified tax declaration in the absence of activity is filed after the reporting period (quarter, six months 9 months, after the end of the year), no later than the 20th day of the month that follows the reporting one.

Reporting is submitted to the tax office:

- For individual entrepreneurs - at the place of registration (registration).

- For organizations - at the location indicated in the constituent documents.

How to submit a single declaration to the Federal Tax Service Inspectorate in 2015-2016

Today, there are three options for filing these reports:

- On paper, for this it is necessary to provide it to the INFS either in person or through a representative. You should prepare 2 copies - 1 copy for the tax office, and keep the second one with a mark of acceptance - you will need it to confirm the fact of delivery.

- With the help of Russian mail, a valuable letter with a list of attachments and, preferably, with a declared value. The date of acceptance of the envelope by the post office employees will be considered the date of delivery to the tax office.

- With the help of services for electronic submission of documents via the Internet, under the agreement of Electronic Document Management.

Attention! When filing a declaration through a representative (trustee), you will need a power of attorney issued by you.

Filling out a single simplified tax return sample

The document consists of two sheets:

- Title page.

- A sheet containing information about the taxpayer.

What you need to know when filling out the declaration:

- The declaration must be completed with a fountain pen, ballpoint pen, blue or black ink, or it can be printed on a printer or typewriter.

- If a mistake is made in the document, then correction by a proofreader or erasure is not allowed.

- To correct the error, it is performed in the following order: the incorrect value is crossed out, a new one is entered, and after that it is necessary to put the date of the amendment and the certifying signature of the person who will sign the declaration next to it.

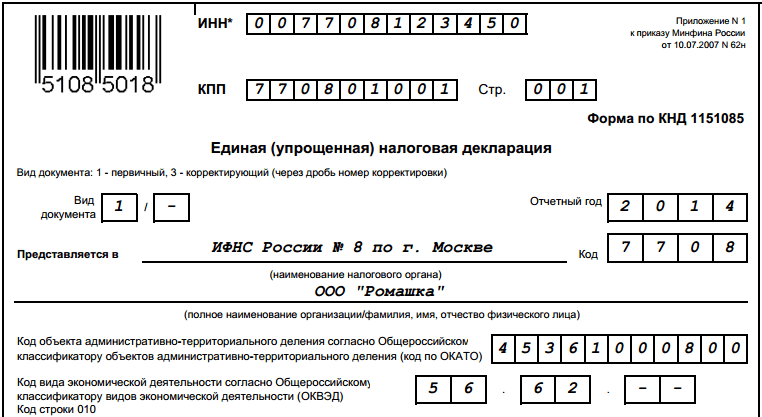

- On each sheet of the upper part, it is necessary to write down the TIN and, if there is a checkpoint of the organization (IP). If the TIN contains 10 characters, then zeros are put in the first two cells.

Sample filling the first (title) page

When filling out the column type of document, the following values are entered:

- In the case of submission of the primary report, "1" is put in the first cell, the adjacent cell remains empty

- When filing a corrective tax return, according to which a correction is made to a previously submitted report, the number “3” is put in the left square, and the number of the correction, say, “1”, “2 ″, etc., in the right one. so for the first correction report 3/1 is indicated

- Reporting period for which reporting is provided.

- The full name of the Federal Tax Service, where the data is provided, its code, consists of 4 digits, for example, the Federal Tax Service Inspectorate No. 66 in Moscow - 7766.

- Full name of the organization (individual entrepreneur) in accordance with the registration documents, without abbreviation.

- Further, in the OKATO column, it is necessary to write down the OKTMO code, according to the changes from January 1, 2014. We begin to write down from the beginning, if there are still empty cells to the end of the field, we put down zeros.

- In the OKVED field, a four-digit code number is indicated, which is indicated in the registration documents as the main type of activity.

After that, you must provide information about zero taxes:

- The name of the tax is indicated.

- Further, the chapter of the tax code corresponding to the specified tax is indicated, while taxes must be indicated in accordance with the order of the chapters of the Tax Code. For example, VAT is indicated first, chapter 21, and after income tax, chapter 25 of the Tax Code.

- Next, you must indicate the tax period for the relevant tax for which the data is provided. When submitting for a quarter, the figure "03" is indicated, when submitting for half a year - "06", for nine months - "09" and when reporting for a year - "0". Quarter numbers are recorded by their numbers - "01" first, "02", "03" and for the fourth - "04".

If the reporting period is a quarter (6 or 9 months), and the tax period is a calendar year, in this case, the corresponding period is indicated in column 3, and column 4 remains blank.

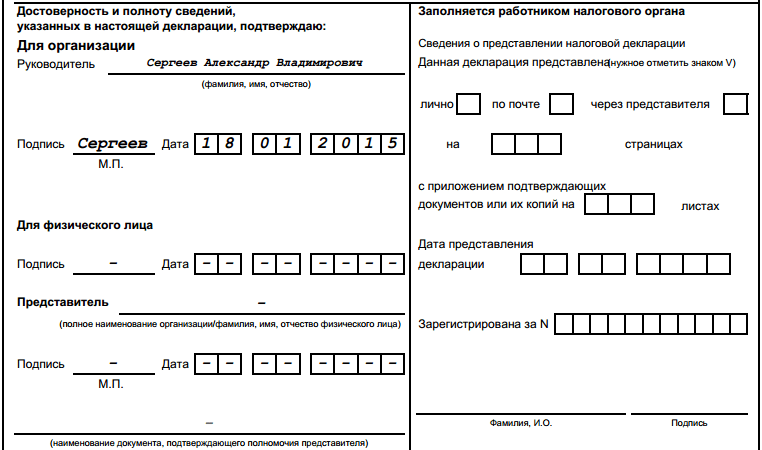

Below is the contact phone number of the taxpayer, the number of pages of the declaration, as well as the number of supporting documents, if any, are submitted with the declaration.

At the end, the data on the person confirming the report is filled in, in the case of the head - the full name, his signature and the date of approval are affixed, a seal is affixed (if the taxpayer uses it in economic activity). If a document is signed by an authorized person, in addition to his full name and signature, it is necessary to indicate the data of the power of attorney on the basis of which he acts.

The field for an employee of the tax authority remains blank.

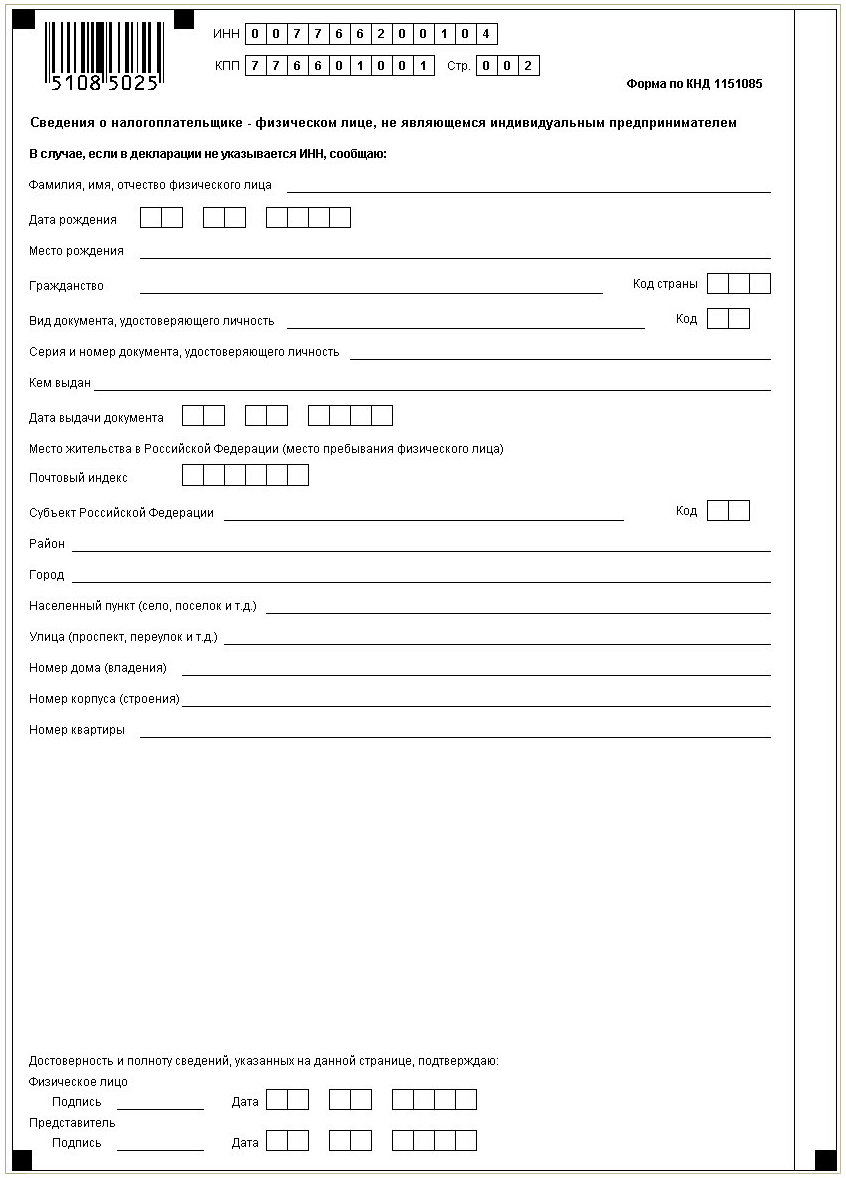

Sample filling out the second sheet of a single declaration

The second sheet is required to be filled out by an individual who is not an individual entrepreneur and does not have a TIN. There shouldn't be any special difficulties.

All data is filled in on the basis of an identity document, the code of which is:

- Birth certificate, applied for persons under 14 years of age - "03".

- Foreigner's passport - "10".

- When filling out on the basis of a residence permit in the Russian Federation - "12".

- Temporary identity card issued in the form 2P - "14".

- Based on the passport of a citizen of the Russian Federation - "21".

- Birth certificate issued abroad - "23".

Procedure if a single simplified declaration is submitted by mistake

There are such situations if a single declaration was submitted, and then the movement of money was detected in the current account or cash desk for the submitted reporting period, or an object of taxation was identified, what should be done in this case?

It is necessary to submit revised declarations for the taxes reflected in the single declaration, the correction number will be 1, because a single declaration will be considered the primary report. A revised report is not submitted for a single declaration. Based on the letter of the Ministry of Finance No. 03-02-07 / 2-154 of 12.11.2012, and letter No. 03-02-07 / 1-243 of 08.10.2012, as well as on the basis of the opinion of the courts (by order of the Federal Antimonopoly Service of the Moscow District No. -A41 / 7687-11 dated 07/29/2011).

Download the form of a single simplified declaration