Main details of 6-NDFL filing on paper

As you know, in accordance with the current legislation, it is possible to submit tax reports in two forms - in electronic or on paper.

At the same time, it is worth noting the fact that not all taxpayers are given the opportunity to independently choose one of the two above options, and to obtain it, it is necessary that the activity meets certain conditions.

Dear Readers! The article talks about typical ways of solving legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and WITHOUT DAYS.

It's fast and IS FREE!

In addition, it is necessary to take into account the fact that the submission of 6-NDFL on paper provides for a lot of its peculiarities that need to be taken into account in the process of preparing such reports.

The problem of choice, the ability to take electronically

In accordance with paragraph 3 of Article 230 of the Tax Code, taxpayers must file reports on the calculated and withheld amounts of personal income tax in paper or electronic form, and each of the above options has its own conditions and rules for filing.

The electronic format is provided, in principle, for any legal entities that have the status of tax agents, and such reports must be sent using Internet channels through the official website of the Tax Service. The electronic option for filing reports is specified in Appendix No. 3 to the order of the Tax Service No. ММВ-7-11 / 450.

The preparation of this form is carried out using the free service "Legal entity taxpayer", which is downloaded from the official website of the tax authority. At the same time, when sending reports in electronic format, legal entities may not worry about this and check the correctness of the format, because the operator through which the transfer is carried out will have to ensure the reliability of all documents.

If the 6-NDFL form in the process of sending passed all the options for automatic verification, then in this case the program skipped the specified format, and therefore accountants should not worry about the inconsistency of any data.

Paperwork for reporting is provided only for certain categories of legal entities, and in particular, this applies to those employers who, during the reporting period, had a number of employees within 24 people. The total number of employees is reflected in line 060 of the first section of the 6-NDFL form.

Filling without errors

Reporting under 6-NDFL represents another test for accountants, although recently representatives of the tax authorities have repeatedly talked about what needs to be taken into account in the process of drawing up such documentation and what errors need to be taken into account.

Thus, the main mistakes made by authorized persons during the previous reporting campaign can be summarized as follows:

- complete absence or inaccurate filling of certain points, which should indicate information about the full name of the reporting company, invalid and other information;

- incorrect indication of the rate and amount of tax used, as well as the total number of persons from whose income personal income tax is collected;

- incorrect indication of the date of actual receipt of income of individuals, as well as the calculation and transfer of tax withheld from these amounts.

At the same time, it is worth noting that when preparing paper reports, there are also several of their own mistakes, in connection with which tax officials pay attention to the key nuances of drawing up such documents. First of all, this concerns the possibility of compiling such reports only for those companies in which the number of employees does not exceed 24 people, as well as the fact that the recommended font for compiling such reports is Courier New with a size of 16 or 18 points.

It is separately indicated that it is important to observe the exact dimensions of the values and the location of the details, and making any adjustments to them is strictly prohibited. At the same time, for those who pass 6-NDFL on paper, some indulgences are provided, and in particular, it is possible not to put dashes in the blank cells, and the numerical values can be aligned according to the last paragraph.

The reports drawn up in paper form will not be accepted by the employees of the control bodies if, during the reporting period, the company made payments in favor of more than 25 individuals.

Where and in what time frame to take

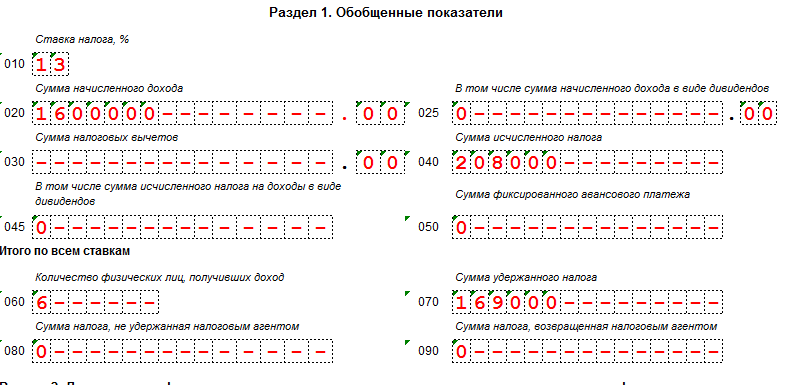

The form and procedure for issuing 6-NDFL is clearly indicated in the order of the Tax Service No. ММВ [email protected] which was published on October 14, 2019. At the same time, it is worth noting the fact that the principle of preparing calculations did not undergo any changes in 2019 and is not much different from tax returns. Thus, the first sheet is the title page, on the second you need to indicate the total tax amount and its calculations, as well as the amount of profit with payment dates, all kinds of deductions and those tax amounts that were withheld from salaries.

In the calculation of a particular organization, there may be not two, but a larger number of sheets, for example, if employees' profits are subject to several different rates, or if companies do not have enough lines to fill in profits with payment dates. In such a situation, it will be necessary to fill out several sections at once with the calculation of the tax amount or the profit paid.

Any employers and private entrepreneurs who use the labor of hired employees need to submit such reports to the tax service, and it does not negate the need to submit certificates in the 2-NDFL form, and legal entities need to submit both.

In particular, 6-NDFL reflects the calculated and withheld tax as a whole, while the 2-NDFL form reflects the amount of tax that is withheld from each employee.

Calculations must be submitted to the tax office before the last day of the month that follows the reporting period, and it should be noted right away that in this case the deadline for submitting reports does not in any way depend on the form used.

In other words, for both paper and electronic forms, the reporting deadlines are identical:

- first quarter;

- half a year;

- nine month.

If it happened that the deadline date falls on a holiday or a day off non-working day, then in this case, the submission of reports should be carried out on the next working day.

Thus, in 2019, the deadlines for filing reports in the 6-NDFL form are as follows:

As mentioned above, paper reports can be submitted if the average number of employees is less than 25 people, and the company has the right to independently choose which of the options is more convenient for it.

6-NDFL conditions on paper

As a general rule, personal income tax reporting is submitted electronically using telecommunication channels, that is, the company must carry out the following series of operations as standard:

- Sign an agreement with a special telecom operator.

- Provide files with calculations using the official website of the Tax Service.

- Download the free program "Taxpayer LE" from the official website of the service and use it to prepare reports in the form of 6-NDFL.

On paper, the filing of reports is provided only for certain categories of persons who have less than 25 employees on their staff who receive any income. It is necessary to submit reports at the end of each quarter, and all indicators are drawn up on an accrual basis. Thus, when submitting reports after the second quarter, it is necessary to indicate all indicators for half a year, and after the third - yes, the past nine months.

Even if an employee who was paid a salary worked in the company for at least one day, in the future it will have to file reports for the rest of the year, since each report contains data for the entire past year.

For example, the company paid profits to its employees during 01.01.2017-30.06.2017, and there were 23 individuals in total. In such a situation, in accordance with the norms of the current legislation, the organization is given the opportunity to submit its reports in paper form.

At the same time, for example, if in the period from 01.07.2017 to 30.09.2017 she pays profit to several more new individuals (for example, 12 people will receive payments from her), then in this case, submit reports for the past nine months in the form 6-NDFL, it will already have to be exclusively in electronic format, since the total number of individuals receiving income from it will already be 35 people at that time. In addition, for a full year, reports will also be submitted only in electronic form.

Delay penalties

To date, the current legislation provides for three types of liability for this type of reporting:

- for providing incorrect information (making mistakes in the preparation of documentation);

- for filing reports in the wrong form (filing reports in paper form in the absence of such an opportunity);

- for violation of the deadlines for submitting information established by the current legislation.

First of all, it is worth noting the administrative fine that is imposed on the company in case of late delivery of 6-NDFL, and it is 1000 rubles for each missed month, regardless of whether it is full or not. A similar fine is also paid in case of mistakes, and this amount is spelled out in article 126 of the Tax Code.

Tax officials calculate the late payment penalty starting from the day that goes beyond the deadline for filing a return under the Tax Code. In this case, any errors made in the reporting process are meant as inaccurate information. This instruction was spelled out in the official letter of the Tax Service No.GD-4-11 / 14515, published on August 9, 2019.

However, it should be noted that in the official letter No. BS-4-11 / [email protected], published already on November 16, 2019, the representatives of the tax authorities changed their mind, and ultimately came to the conclusion that the inspectors have no right to impose administrative fines for any mistakes made in the 6-NDFL reporting process, if these errors did not harm the budget or the interests of an employee of the company.

The administrative fine in case of being late with the calculation of the head of the company ranges from 300 to 500 rubles. At the same time, do not forget that if the deadline for filing the declaration is missed by more than 10 days, then the tax office gets the right to completely block the company's registered current account.

Special attention should be paid to the fact that if the reports are sent in paper form by mail, then in this case the date when the letter was sent with a list of attachments will be considered as the date of submission.

Thus, the penalties for incorrect reporting in the 6-NDFL form are as follows:

| Violation committed | The amount of the fine |

| Errors in the submitted reporting | 500 rubles for each document |

| Submission of reports on paper in the absence of such an opportunity |